OVERVIEW OF MEDICARE LEVY AND MEDICARE LEVY SURCHARGE

An individual who is a resident of Australia at any time during the income year is liable to pay a Medicare levy based on their taxable income. Medicare levy is calculated at 2% of taxable income, subject to some concessions.

Example

For a single taxpayer with a taxable income of $46,875 the Medicare levy for 2022 will be: = $46,875 x 2% = $937.50

The PAYG withholding deducted from an employee’s gross wages is calculated to include tax and Medicare levy. The Medicare levy is not shown separately on the taxpayer’s payslip or Income Statement / PAYG payment summary, but it is shownseparately on the Notice of Assessment issued by the ATO. There is no rounding to the nearest dollar when calculating Medicare levy.

Non-refundable tax offsets, such as SAPTO, LITO and LMITO cannot be used to reduce the Medicare levy.

While most resident taxpayers will pay Medicare levy at a rate of 2% of their taxable income, there are some concessions available:

- Medicare Levy Reduction

o Individual low income earners will be entitled to a reduction in Medicare levy

o Taxpayers whose family income is low (i.e. couples, with or without dependent children, and sole parents) may beentitled to a reduction in Medicare Levy based on their family income (this will be in addition to any reduction

based on their individual taxable income).

- Medicare Levy Exemption

o Certain taxpayers (prescribed persons) may be entitled to a full or partial exemption from the Medicare levy.

In addition to the Medicare levy, high income earners may be liable for the Medicare levy surcharge if they, and all their dependants, do not have adequate private hospital cover. This is calculated at 1%, 1.25% or 1.5% of surcharge income. This is payable in addition to the basic 2% Medicare levy.

Liability for Medicare levy and Medicare levy surcharge, as well as entitlement to a Medicare levy exemption, may be impacted by whether a taxpayer has any dependants.

DEPENDANT FOR MEDICARE PURPOSES

For Medicare purposes, a person is a dependant of a taxpayer if the person is a resident of Australia for tax purposes, the taxpayer contributes to their maintenance and the person is either the spouse of the taxpayer or a dependent child or student (as defined above).

A spouse includes a partner in a married or de facto relationship.

For Medicare levy purposes, a person whose spouse has died during the income year and who has not remarried will be treated as married as at the end of the year. A couple who has separated (and remain separated as at the end of the income year) will be treated as not being married at the end of the year.

A dependent child or student means:

• A student who is under 25 years and is a full-time student at school, college or university • Any child under 21 who is not a full-time student

A child includes the individual’s adopted child, stepchild, ex-nuptial child, spouse’s child or a child of the individual within the meaning of the Family Law Act 1975.

In addition, there are other criteria that need to be satisfied for a child or student to be classed as a dependant. These criteriadiffer, depending on whether it is the Medicare levy reduction, exemption or surcharge you are considering.

In particular, for a child or student to be classed as a dependant, there may be income tests to be satisfied. Where they apply, they are based on the child’s or student’s adjusted taxable income (ATI). For some concessions, the dependent child or student must be classed as a notional dependant of the taxpayer. That is, the taxpayer must be entitled to at least $1 of the notional tax offset for the child or student.

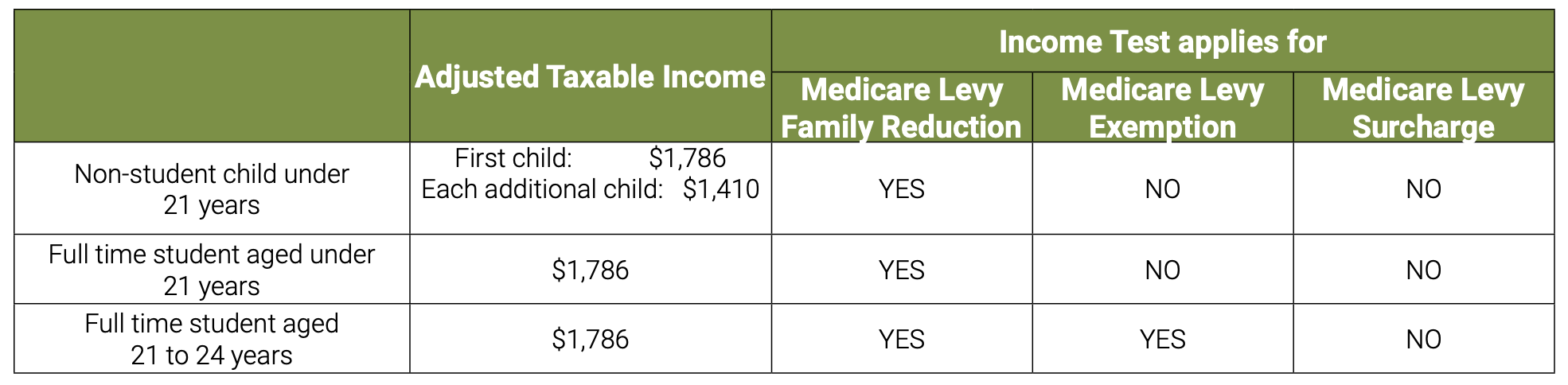

The table below outlines the income tests for dependants for Medicare levy reduction, Medicare levy exemption and Medicare levy surcharge purposes. Where the income tests apply, to be considered a dependant, the ATI of the child or student must be below the income thresholds in the second column.

If the child or student is not a dependant for the whole income year, the above ATI threshold is apportioned on a weekly basis for income above $282.

MEDICARE LEVY REDUCTION

Low income earners & Medicare levy

Relief from paying the Medicare levy is available for low income earning taxpayers whose taxable income falls below various threshold amounts.

A reduction is NOT an exemption to the levy. It is based on taxable income

Calculating Reduced Medicare Levy for Individual Low Income Earners

The levy shades in at the rate of 10 cents for every dollar above the lower threshold amount. If income is greater than the upper threshold, the taxpayer pays 2% of the total taxable income.

Example

Hector has a taxable income of $24,961. His Medicare levy will be calculated as:

- = ($24,961 – $23,365) x 10%

- = $1,596 x 10% = $159.60

No action is required on the tax return for a single taxpayer because this reduction is based entirely on taxable income and the ATO will apply the reduction automatically.