THE DIFFERENCE BETWEEN A DEDUCTION AND A TAX OFFSET AND A DEDUCTION

DEDUCTIONS

A taxpayer’s assessable income is reduced by allowable deductions to calculate their taxable income. The actual tax saving generated by a

deduction does not equal the amount of the deduction. The tax saving will be determined by the taxpayer’s level of income and their marginal tax

rate. The approximate tax saving will vary – from 0, for those below the tax-free threshold, up to 47 cents in the dollar (including the basic Medicare

levy).

Example

Nick has gross income of $130,000 with $1,000 of deductions. The tax and basic Medicare levy payable on his gross income and net income is

calculated as follows:

Tax and Medicare without deductions Tax and Medicare with deductions

Gross Income $130,000 Net Income $129,000

Tax on gross income $ 33,167 Tax on net income $ 32,797

Plus Medicare levy $ 2,600 Plus Medicare levy $ 2,580

Total amount payable $ 35,767 Total amount payable $ 35,377

Nick’s $1,000 deduction has provided him with a tax saving of $390

TAX OFFSETS

A taxpayer’s gross tax on taxable income is reduced by a tax offset on a dollar for dollar basis. Generally, tax offsets are not refundable and are

applied before the Medicare levy. They can only be used to reduce tax payable

If the taxpayer’s non-refundable tax offsets are greater than the tax on their taxable income, the tax offset will be limited to the tax payable. Non-refundable tax offsets cannot be used to reduce the Medicare Levy.

Some tax offsets are refundable and can reduce the Medicare levy as well; note the order that non-refundable offsets, refundable offsets and Medicare is applied. In particular, the Private Health Insurance Tax Offset is a refundable tax offset.

Tax Offsets

LOW INCOME TAX OFFSET (LITO)

For the 2021 and later years, a low income tax offset of $700 is available to Australian resident taxpayers whose taxable income does not exceed $37,500. For taxpayers with taxable income of from $37,501 to $66,666, a reduced low income tax offset is available.

No action is required on the tax return. This offset is calculated automatically by the ATO and is based only on the taxable income.

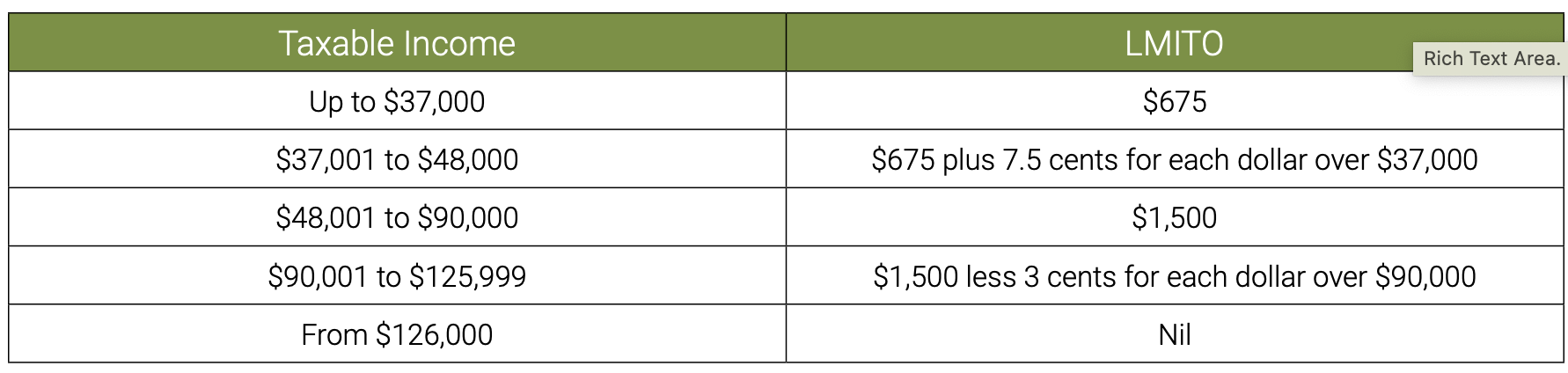

LOW AND MIDDLE INCOME TAX OFFSET (LMITO)

For the 2019 to 2022 years, a Low and Middle Income Tax Offset (LMITO) is available. This offset is in addition to the Low Income Tax Offset and, like the LITO, is a non-refundable tax offset. For the 2022 year, the LMITO is calculated as follows:

No action is required on the tax return. This offset is calculated automatically by the ATO and is based only on the taxable income.

From the 1 July 2022, the LMITO will cease.

BENEFICIARY TAX OFFSET

A tax offset is allowable to recipients of a taxable allowance or benefit from Centrelink or other income that is included at Item 5 of the tax return (e.g. CDEP Payment). This tax offset is designed to minimise the tax payable on the benefit. The offset only applies to the amount of benefit or allowance in EXCESS of $6,000.

Since the actual tax-free threshold is $18,200, this offset will mean the taxpayer will generally not have to pay any tax on theirbenefit. If they have earned any other assessable income during the year, this offset may be insufficient to ensure that they have no tax to pay on their total taxable income.

No action is required on the tax return. The offset will be automatically calculated where the benefit exceeds $6,000. Where the benefit received is not more than $45,000, the following formula applies:

= 0.15 x (taxable benefit – $6,000)

Example

Mark received a taxable benefit of $17,000. His tax offset amount will be:

Tax offset = 0.15 x ($17,000 – $6,000) = 0.15 x $11,000

= $1,650

If the benefit amount exceeds $45,000, the formula is:

= 0.15 x (taxable benefit – $6,000) + 0.15 x (taxable benefit – $45,000)

Example

Joe received a taxable benefit of $48,000. His tax offset amount will be:

Tax offset = 0.15 x ($48,000 – $6,000) + 0.15 x ($48,000 – $45,000) = $6,300 + $450

= $6,750

If the offset amount exceeds the actual tax payable then only an amount equal to the tax payable will be allowed as a rebate. It is a non-refundable offset.

Some software (including Handitax) may calculate this offset incorrectly where the amount included at Item 5 is over $37,000. It is unlikely an amount in excess of $37,000 would be included at Item 5 of the tax return.

LUMP SUM A TAX OFFSET

The tax on a Lump Sum A payment is limited to 30% (plus Medicare if applicable). Therefore, if the taxpayer’s marginal rate of tax is more than 30% a tax offset is calculated to bring the amount of tax on the lump sum back to the correct figure.

Example

Ron’s taxable income is $89,000 and his marginal rate of tax is 32.5 cents in the dollar. Included in his income is a Lump Sum A (Item 3R) of $4,000. Lump Sum A payments have a maximum rate of tax of 30 cents in the dollar. Therefore, Ron is entitled to a lump sum tax offset of 2.5 cents in the dollar on the Lump Sum A amount (i.e. 0.325 – 0.30 = 0.025).

Ron’s lump sum tax offset is:

= $4,000 x 0.025 = $100

On the Notice of Assessment, the ATO will calculate the tax payable at ordinary rates and apply a tax offset to reduce this to the correct amount.

Method of Calculating Lump Sum A Tax Offset

The offset is calculated using the following steps:

• Calculate tax on taxable income (A)

• Subtract Lump Sum A from taxable income to arrive at residual taxable income • Calculate tax on residual taxable income

• Calculate tax on Lump Sum A at appropriate rate

• Add together tax on residual taxable income and tax on Lump Sum (B)

• Subtract (B) from (A) to arrive at the Lump Sum A tax offset

If the example of Ron, above, the tax offset is calculated as follows:

axontaxableincomeof Less Lump Sum A Residual taxable income Plus $4,000 x 30% LUMP SUM A TAX OFFSET

89,000 4,000 85,000

Tax on residual income

18,092.00 1,200.00

19,392.00 (A)

19,292.00 (B)

100.00

If Ron’s taxable income had been less than $45,000, and his marginal tax rate was 19%, he would not be entitled to a lump sum tax offset for his Lump Sum A payment.

No action is required on the tax return. This offset is calculated automatically by the ATO from the information already reported on the tax return.

NOTE

No tax offset applies to Lump Sum B or D. These lump sums are already treated concessionally (i.e. tax is not payable on the full amount received).

Rebate income & SAPTO

ITEM T1 – SENIORS AND PENSIONERS TAX OFFSET

The non-refundable Seniors and Pensioners Tax Offset (SAPTO) is available to a person who has rebate income below the relevant threshold amount and:

EITHER

- Has an amount of assessable income that is included at Item 6 of the tax return – e.g. social security pension (including single parenting payment), an education entry payment, service pension, carer service pension, income support supplement or Defence Force Income Support Allowance or DFISA-like payment OR

- Qualifies for the age pension under the Social Security Act 1991 on at least one day in the income year OR

- Qualifies for an age pension, allowance or benefit under the Veterans’ Entitlements Act 1986 on at least one day of the

income year (other than under the Veterans’ Children Education Scheme)

Any person who is in prison for the whole income year does not qualify for this offset.If the taxpayer is entitled to both the beneficiary tax offset and the Seniors and Pensioners Tax Offset, they will only receive the one that gives the higher tax offset.

NOTE

If the taxpayer is eligible for an age pension under either the Social Security Act 1991 or the Veterans’ Entitlement Act 1986,they do not actually need to be receiving these payments to be able to claim SAPTO.

- To qualify for the age pension under the Social Security Act 1991 the taxpayer must firstly satisfy the age test.

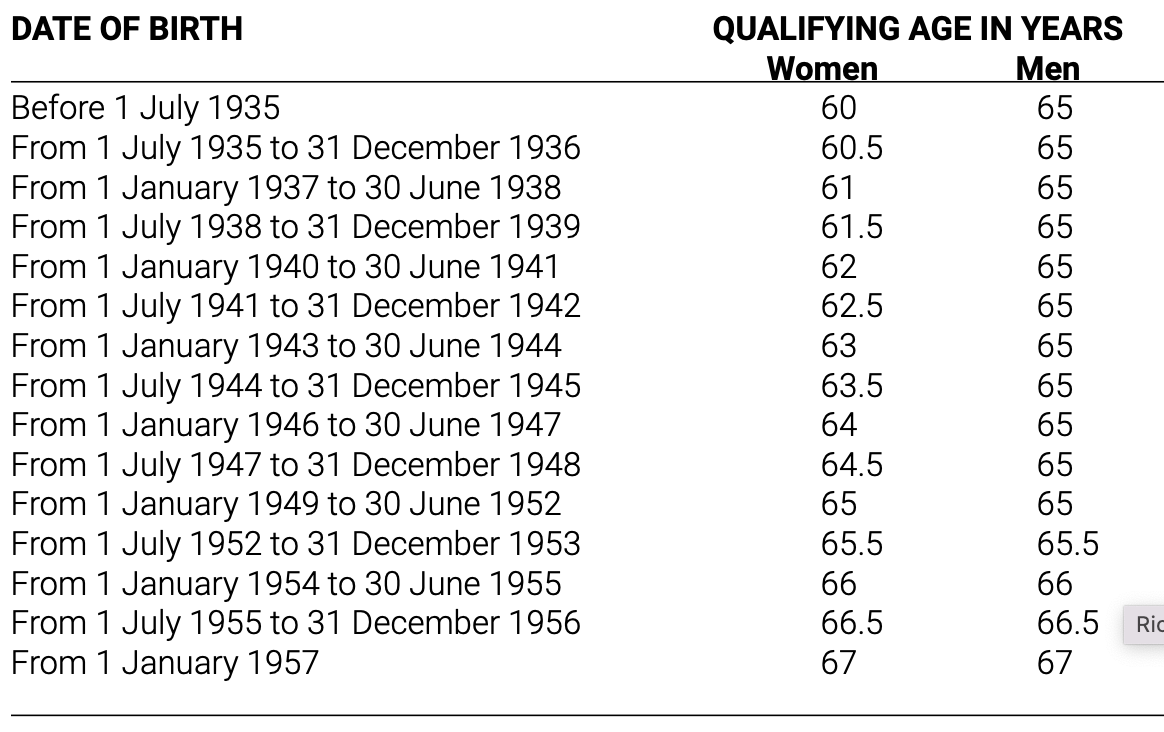

The age at which a person qualifies for the age pension has changed over the years. From 1 July 2023, both men and women will have to be 67 in order to qualify for the pension. However, this change is being phased in over a number of years. The phase-in schedule (from the 2010 year) is shown in the following table.