The first step in calculating a taxpayer’s tax refund or tax payable is to calculate their taxable income. Taxable income is the taxpayer’s assessable income less allowable deductions and is the income on which tax is payable. The tax return must be completed to arrive at this figure.

The tax rates will vary depending on the taxpayer’s residency status – resident or foreign resident. In this course we will generally be considering taxpayers that are residents of Australian for tax purposes.

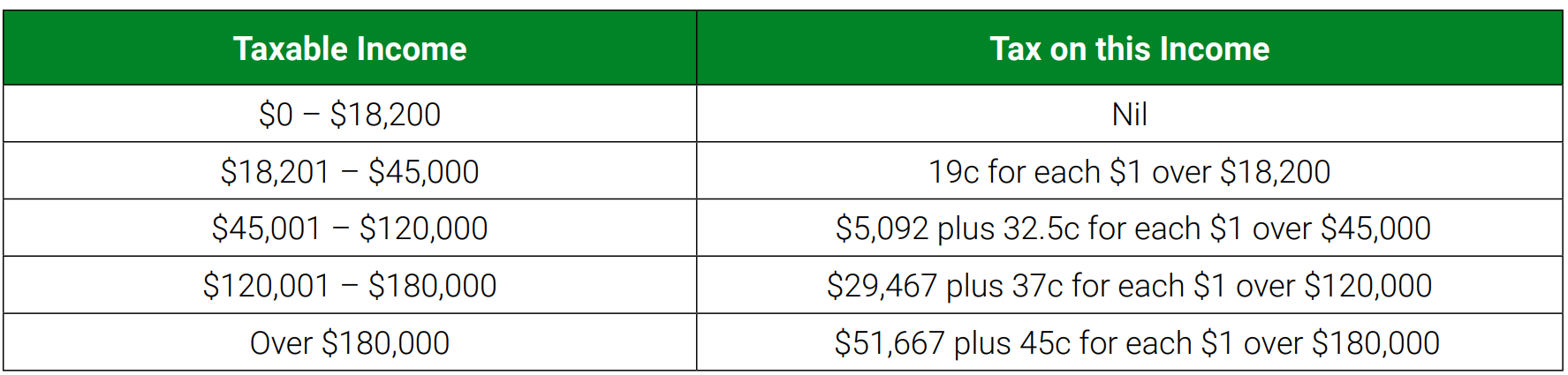

RESIDENT TAX RATES

Tax-Free Threshold

Australian resident taxpayers are entitled to the tax-free threshold, which is currently $18,200. This means that for the first $18,200 of taxable income there is no tax payable. Taxable income in excess of the tax-free threshold is taxed at progressive rates of tax, as shown in the table below.

A taxpayer whose income falls into the top marginal rate of 45 cents will not pay that amount for every dollar of their taxable income. They will still be entitled to the tax-free threshold, and the lower tax rates on the relevant portion of their income; they will only pay at the rate of 45% on the amount above $180,000.

RESIDENT TAX RATES 2022-23

FOREIGN RESIDENT TAX RATES

A taxpayer who has been a foreign resident (but not a working holiday maker) for tax purposes for the full year will not be entitled to the tax-free threshold and will pay tax at the following rates:

NON RESIDENT TAX RATES 2022-23

CHANGE OF RESIDENCY STATUS

The tax rates are different for residents and foreign residents. The front cover of the tax return should indicate whether the taxpayer is a resident for tax purposes or not. When applying the tax rates, only the resident tax rate or the foreign resident tax rate can be applied for any particular year. If the taxpayer changes residency status during the year (i.e. they are a resident for part of the year and a foreign resident for part of the year) the return should indicate they are a resident and the resident tax rates will be used. However, the taxpayer will have a reduced tax-free threshold applied, based on the number of months they were a resident for tax purposes.

For a taxpayer who changes residency status during the year, the adjusted tax-free threshold will have two components:

• the first is a flat amount of $13,464

• the second is the additional $4,736 apportioned over the number of months they have been a resident during the income year, including the month they arrived or departed.

WORKING HOLIDAY MAKERS

A working holiday maker (WHM) is a person who has a visa subclass

• 417 (Working Holiday)

• 462 (Work and Holiday).

Both of these visas are open to people aged between 18 and 30 years of age (in some cases 35 years of age) from eligible countries to enable them to holiday and work or study in Australia. The visas are for 12 months but may be extended to a second and third 12 month visa.

For most working holiday makers, the first $45,000 of their income is taxed at 15% and the balance is taxed at ordinary tax rates (an exception

to this is outlined below).

WORKING HOLIDAY MAKER TAX RATES 2022-23

As the marginal tax rate is the same on income over $45,000 irrespective of whether a taxpayer is a resident or a foreign resident, all affected

working holiday makers will pay the same rate of tax. It is still important to correctly determine the residency status of working holiday makers,

as there will be other factors to consider, such as Medicare and eligibility for tax offsets. These will be covered in a later module.

Employers of working holiday makers are required to register with the ATO as an employer of working holiday makers and withhold tax at this

rate.

If working holiday maker has income of less than $45,001 and has had tax withheld at the correct rate from this income, they will not be

required to lodge a tax return or advise the ATO they are not lodging.

TAXPAYERS TO WHOM THE WHM TAX RATES DO NOT APPLY

Some of Australia’s double tax agreements contain a non-discrimination article (NDA) that states that nationals of these countries shall not be

subject to tax in Australia that is more burdensome than is imposed on Australian nationals in the same circumstances. As such, the WHM tax

rates do not apply to WHMs from these countries who are residents of Australia for tax purposes. These taxpayers will be taxed at ordinary tax

rates for residents.

96

This will only apply to WHMs who are residents of Australia for tax purposes and are from Chile, Finland, Germany (for the 2018 and later

years), Japan, Norway, Turkey, the United Kingdom and Israel (for the 2021 and later years).

Employers of WHMs will continue to withhold tax at the working holiday maker tax rate. Where a WHM is a resident for tax purposes and is

from a NDA country, they will be able to lodge a tax return and obtain a refund of any additional tax withheld. Alternatively, they may be eligible

to apply for a PAYG variation to vary the amount of tax the employer withholds from their wages.

INCLUDING WHM INCOME IN THE TAX RETURN

Wages earned by a working holiday maker will be included separately on the Income Statement. This income is included at Item 1 of the tax

return, along with the Code H. Any other assessable income (e.g. interest) earned while the taxpayer is a working holiday maker is included

at the relevant section of the tax return, and allowable deductions can be claimed under the usual rules. The taxable working holiday maker

income is then included at Item A4 of the tax return, as well as the home country of the taxpayer.

The amount included at Item A4 will be the taxable income earned during the year while a working holiday maker from all Australian sources

– wages, business income, interest etc. This will enable the ATO to calculate the tax at the correct rate. When preparing tax returns on the

software, any amount shown on an Income Statement with Code H will automatically be transferred to Item A4. This will need to be adjusted if

there is income other than wages or if there are tax deductions to be taken into consideration.

BRIDGING VISAS

If a working holiday maker applies for another WHM visa while in Australia, they may be granted a bridging visa which would allow them to

stay in Australia after the first WHM visa expires and while waiting for the decision to be made on the new visa. During the period they are on

the bridging visa, they will still be classed as and taxed as a working holiday maker.

However, if a working holiday maker has applied for a visa other than a WHM visa (for example an employer sponsored visa), and they are on

a bridging visa awaiting a decision on the new visa, once the WHM visa expires they will not be subject to the WHM rates of tax. Their tax rate

will be determined by their residency status.

COVID 19 PANDEMIC EVENT SUBCLASS 408 VISA

This visa was introduced during the COVID 19 pandemic for people living and working in Australia on temporary visas that are about to expire.

They are specifically aimed at those working in critical sectors to the Australian government who can’t go home due to travel restrictions and

who have no other visa options.

98

The definition of a WHM was amended to include those on a subclass 408 Pandemic event visa if that visa was granted to allow the holder of

a subclass 417 visa or subclass 462 visa to remain in Australia. This legislation applied retrospectively to foreign residents from 1 July 2019

and to residents prospectively from the first 1 July 2022.

As a result, WHMs who are foreign residents for tax purposes will be subject to the WHM tax rates for the period they are on the subclass 408

Pandemic event visa. However, WHM who are residents of Australia for tax purposes (but not from a country from an NDA country) will be

taxed at resident tax rates from the date they move to a 408 Pandemic event visa up to and including 30 June 2022. From 1 July 2022 they will

again be subject to the WHM tax rates.

WHMs who are residents of Australia for tax purposes and from an NDA country will continue to be taxed at resident tax rates while on a 408

Pandemic event visa.

CHANGE OF STATUS

If the taxpayer changes status during the year (from a WHM to another type of visa) only the taxable income earned during the period they

were on the WHM Visa is included at Item A4 and subject to the special tax rates. The remainder of their income is subject to normal tax rates

– resident or foreign resident depending on the taxpayer’s circumstances. If they have had the same employer for both periods, they should

have both WHM income (code H) and non-WHM income on their income statement.

Tax calculations in these circumstances can be complex and you will not be required to do them manually. It is sufficient that you understand

how the calculation works and how to enter the relevant information on the tax return.