If you’re eligible to claim work from home deductions, there are 2 ways you can do this – the fixed rate method or the actual cost method.

What expenses can be deducted for working from home?

Deductions for expenses you incur to work from home such as stationery, energy and office equipment.

Additional running expenses

Running expenses relate to the use of facilities within your home. These expenses are generally considered private and domestic expenses. You can claim a deduction for additional running expenses you incur as a direct result of working from home.

Additional running expenses may include:

- electricity or gas (energy expenses) for heating or cooling and lighting

- home and mobile internet or data expenses

- mobile and home phone expenses

- stationery and office supplies

- the decline in value of depreciating assets you use for work – for example

- office furniture such as chairs and desks

- equipment such as computers, laptops and software

- the repairs and maintenance to depreciating assets.

In limited circumstances where you have a dedicated home office, you may also be able to claim:

- occupancy expenses (such as mortgage interest or rent)

- cleaning expenses.

If your employer pays you an allowance to cover your working from home expenses, you must include it as income in your tax return.

If you’re a sole trader or business owner and your home is your principal place of business, see Deductions for home-based business expenses

Method to calculate work from home deductions

From 1 July 2022 there are 2 methods available to calculate your claim:

Fixed rate method

Summary

- an amount (67 cents) per work hour for additional running expenses

- separate amount for expenses not covered by the fixed rate, such as the decline in value of depreciating assets

- you no longer need a dedicated home office.

Eligibility to claim

To use the fixed rate method, you must:

- incur additional running expenses as a result of working from home

- have a record of the total number of hours you work from home and the expenses you incur while working at home.

How it works

You can claim 67 c for each hour you work from home during the relevant income year. The rate includes the additional running expenses you incur for:

- home and mobile internet or data expenses

- mobile and home phone usage expenses

- electricity and gas (energy expenses) for heating, cooling and lighting

- stationery and computer consumables, such as printer ink and paper.

The rate per work hour (67c) includes the total deductible expenses for the above additional running expenses. If you’re using this method, you can’t claim an additional separate deduction for these expenses.

Actual cost method

- the actual expenses you incur as a result of working from home.

You must keep records to show you incur expenses as a result of working from home. The type of records you need to keep will depend on the method you choose to calculate your expenses.

For a summary of this information in PDF format, see Working from home deduction (PDF, 777 KB)This link will download a file.

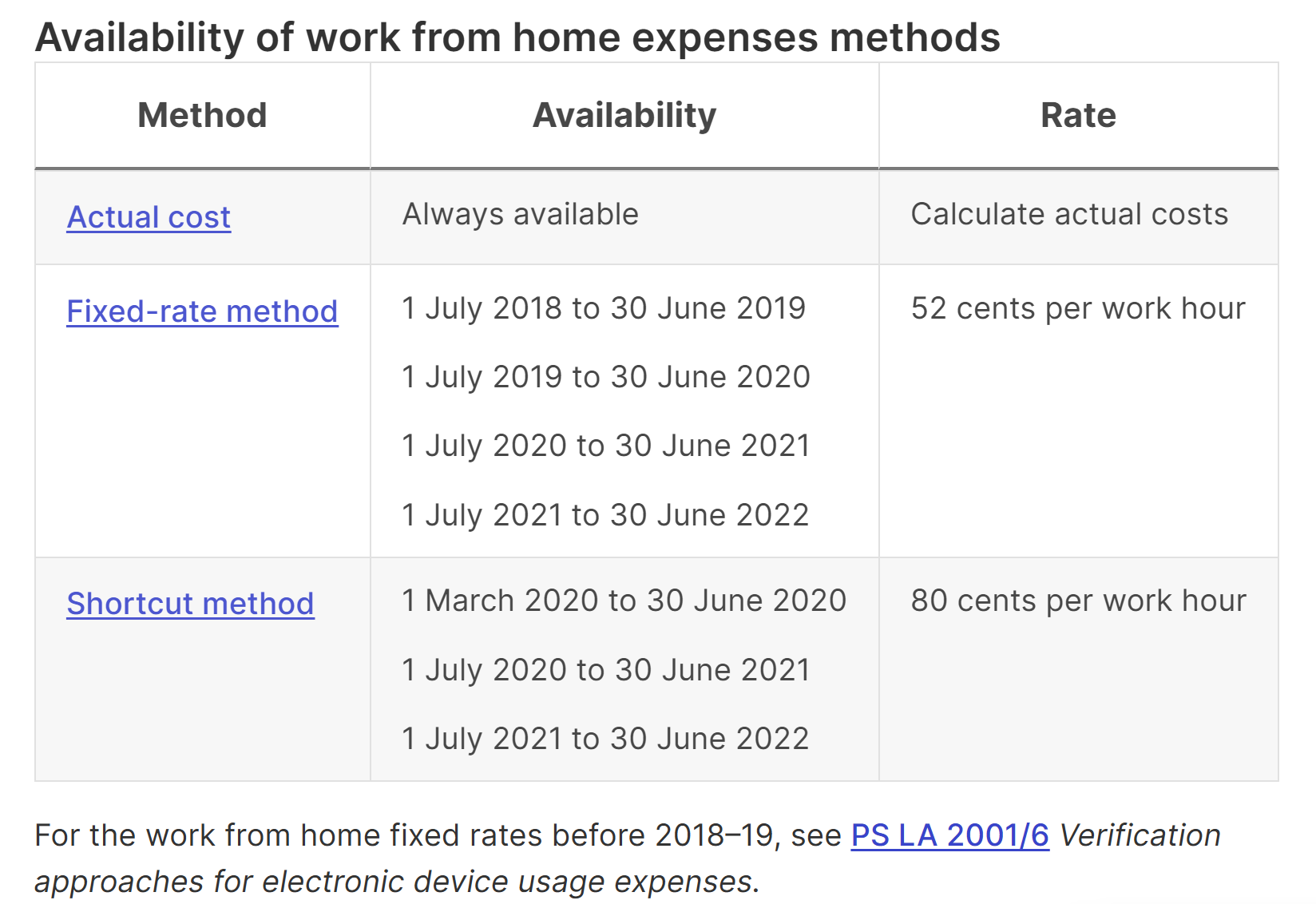

Prior year work from home deductions methods

To work out your deduction for working from home expenses in prior income years, use the table below for the methods available.

Eligibility to claim

To claim working from home expenses, you must:

- be working from home to fulfil your employment duties, not just carrying out minimal tasks, such as occasionally checking emails or taking calls

- incur additional running expenses as a result of working from home

- have records that show you incur these expenses.

To calculate your deduction for working from home expenses, you must use one of the methods set out below.

Where you incur running expenses for both private and work purposes, you need to apportion your deduction. You can only claim the work-related portion as a deduction.

Expenses you can’t claim

You can’t claim a deduction for:

- coffee, tea, milk and other general household items, even if your employer may provide these at work

- costs that relate to your children’s education, such as equipment you buy – for example, iPads and desks, subscriptions for online learning

- items your employer provides – for example, a laptop or a mobile phone

- expenses where your employer reimburses you for the cost.