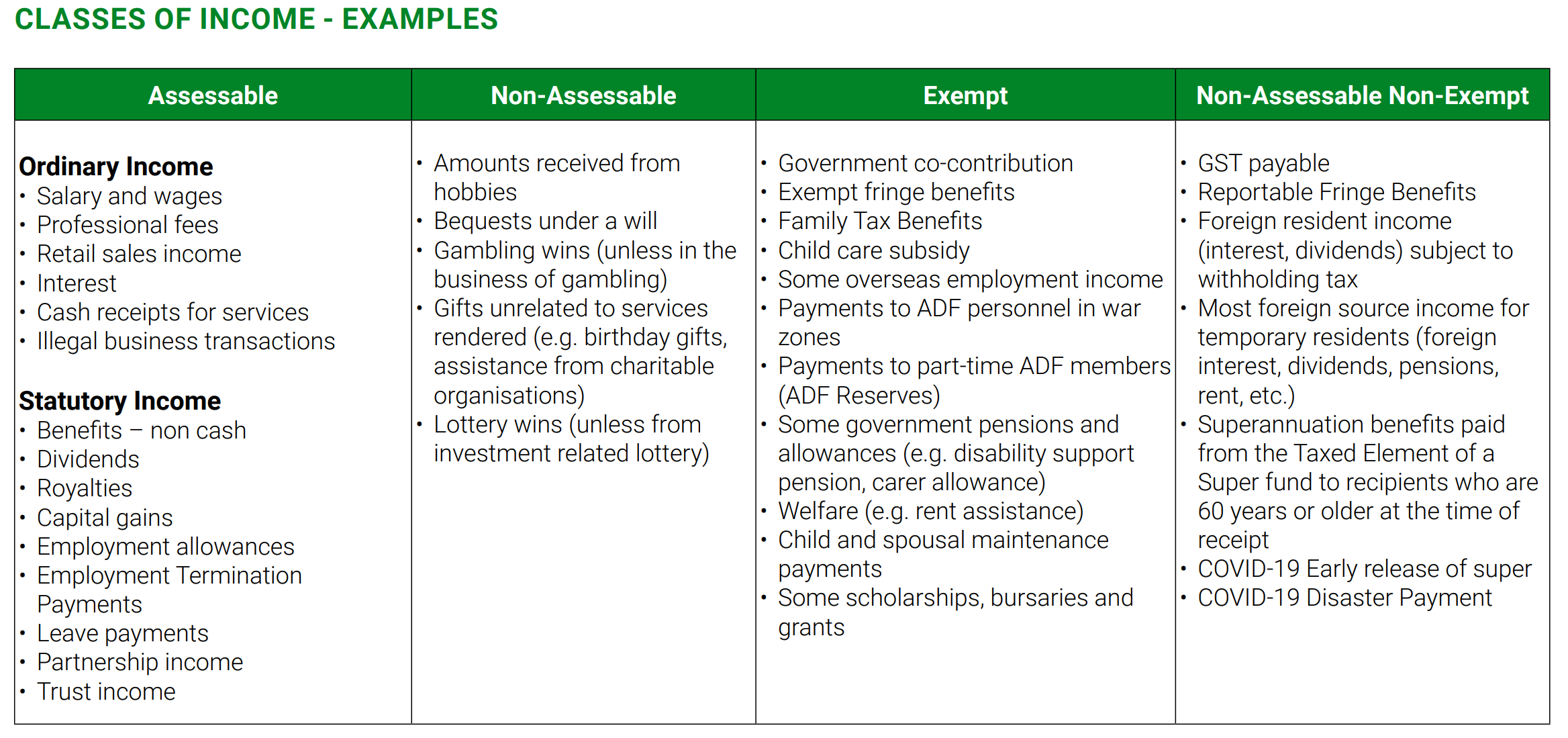

WHAT IS INCOME?

Tax payable is calculated based on taxable income, which is assessable income minus allowable deductions. It is important that you fully

understand the difference between the various types of income, as not all amounts received by a taxpayer will be classed as assessable

income.

Income can be divided into four categories:

• Assessable income

• Non-assessable amounts

• Exempt income

• Non-assessable non-exempt income (NANE)

ASSESSABLE INCOME

Assessable income is the income you will use as the first step in calculating tax. Assessable income is defined in the Income Tax Assessment

Act 1997 (ITAA 1997) Division 6 as ordinary income (income according to ordinary concepts) and statutory income (income which is

specifically included in a provision of the ITAA).

The Income Tax Act does not contain a definition of the word ‘income’. In determining what is classed as ordinary income, reliance must be

placed on general concepts and usage, assisted by current tax rulings and court decisions.

The courts have identified a number of factors which might indicate that an amount has the characteristics of income according to ordinary

concepts. An element of periodicity, recurrence or regularity may indicate that an amount is income in nature.

Examples of amounts that will be considered ordinary income include:

• earnings from the performance of services, such as salary and wages

• amounts are received as a result of carrying on a business, and

• amounts that are received in the nature of a return on capital investment, such as interest, dividends and rents.

16

Items that are not income in nature include:

• capital payments

• loans

• gifts

Even if an amount is not income according to ordinary concepts, it may be assessable income if it is included under a specific provision of the

Income Tax Assessment Act (statutory income).

Examples of statutory income include:

• dividends

• rents

• trust distributions

• lump sum payments such as employment termination payments and some superannuation payments

capital gains

Assessable income may fall into both categories – ordinary income and statutory income – but it is only included in assessable income once.

Generally, it is the specific income provisions which prevail, however in the case of capital gains it is the ordinary income provisions which will

prevail. In some cases, it does not really matter whether the income is included under the ordinary or statutory provisions, but in other cases

the way income is calculated will differ between the provisions. Throughout the course you will learn the taxation treatment of different types

of income.

INCOME VS CAPITAL PAYMENTS

One characteristic of income is an element of periodicity, recurrence or regularity. However, this is only an indicator. In the case of

compensation payments, amounts take on the characteristic of the amount for which they are a replacement.

Whether received as a lump sum or as periodic payments, the following payments will be assessable as ordinary income:

• Payments under an income protection policy

• Weekly workers compensation payments

• Amounts paid to induce a person to return to work or to commence employment

17

The following payments will be capital in nature and not assessable as ordinary income:

• Payments made as compensation for an injury (including psychological and emotional)

• Payments to compensate for pain and suffering as a result of a person being wronged, illness or injury

• Payments to compensate for loss of future earning capacity

EXEMPT INCOME

Exempt income is income which has the characteristics of ordinary income, but which is specifically exempted under the Income Tax

Assessment Act 1997, Section 11 or other Commonwealth Law. Although exempt income is not included in assessable income, it may be

used to reduce tax losses and some exempt pensions are included in certain income tests.

EXAMPLE

A disability support pension has the characteristics of ordinary income, but is specifically made exempt by the ITAA where the recipient is

under age pension age.

NON-ASSESSABLE NON-EXEMPT INCOME (NANE)

NANE income is income that the law expressly says is neither assessable nor exempt. NANE income is ignored when calculating taxable

income and tax losses. Thus, it is effectively treated as if it was never income.

EXAMPLE

The Disaster Recovery Allowance (DRA) is a short-term income support payment available from Services Australia to assist individuals who

can demonstrate that their income has been affected as a direct result of a disaster. Eligible individuals may be eligible for a maximum of 13

weeks payment from the date of the loss of income as a direct result of a disaster.

The DRA has the characteristics of ordinary income and is generally assessable income. However, the DRA received as a result of the

bushfires commencing in Australia in the 2019-20 year were specifically made non-assessable non-exempt income under the ITAA.

Similarly, payments made on or after 1 January 2020 by a State or Territory for the loss of income as a result of an individual performing

volunteer work with a fire service of a State or Territory during 2019-20 have the characteristic of ordinary income but are specifically made

non-assessable non-exempt income under the ITAA.

18

NON-ASSESSABLE AMOUNTS

This includes amounts that are not assessable income, exempt income or non-assessable non-exempt income (NANE) – that is, amounts that

are neither income according to ordinary concepts nor statutory income, so will not be included as income in the tax return.

Examples of non-assessable amounts include:

• rewards or gifts on special occasions, such as cash birthday presents and gifts from relatives given out of love (however, gifts may be

taxable if you receive them as part of a business-like activity or in respect of income-earning activities as an employee or contractor)

• prizes in ordinary lotteries, such as lotto draws and raffles

• prizes in game shows, unless the taxpayer receives regular appearance fees or game-show winnings

• amounts received as a result of an activity that is a hobby rather than a business

• Services Australia income compliance (Robodebt) class action settlement payment

In some cases it may be difficult to determine whether amounts are income in nature and amounts of this type has often been the subject of

an administrative ruling or a legal decision. We will consider the differences between a hobby and a business in a later module.

Another example of non-assessable amounts include payments made to a volunteer carer to cover expenses of providing respite care for a

disabled person (TD 2004/75). Similarly, payments to volunteer foster carers to help meet the costs of providing foster care are not assessable

income (TD 2006/62).

Although both of these types of payments have the regularity of ordinary income, volunteer carers are not paid any amount for their time or

to reward them for any personal services they provide. They are volunteering their time without any expectation of monetary reward. Nor are

they providing the care as an employee, carrying on a business of respite care or being paid any amount to compensate for the loss of other

income. The payments therefore do not have the characteristics of ordinary income.

The payments are considered to be in the nature of a reimbursement of expenses, and are not paid as an allowance or any other kind of

payment in respect of employment or services rendered. As such, they are not included as income under the statutory provisions (s 15-2)

which include allowances, gratuities, bonuses and premiums paid in respect of or in relation to employment or services.

However, where a person is employed as a carer or operating a business of caring, the income earned will be assessable.

19

EXAMPLE FROM TD 2004/75

Peter provides volunteer respite care for a child with disabilities for one weekend (Friday evening to Monday morning) per month. Peter is paid

an amount of $350 for the weekend by an organisation that arranges respite care for disabled persons. The payment is intended to cover

expenses incurred in providing the respite care including food and drink, laundry, recreation activities and transport. The payment is considered

to be in the nature of a reimbursement of expenses and therefore is not included in Peter’s assessable income.