Government Payments

Whilst some government payments are exempt income or non-assessable non-exempt income, many of these payments are assessable.

Assessable government payments may be included at Items 1, 5, 6 or 24 of the Income Tax Return, depending on the type of payment. It is

important these amounts are included at the correct item, as this will determine the taxpayer’s entitlement to particular tax offsets.

Certain exempt pensions are included in the Income Test section of the tax return (at Item IT3). Although these amounts are not taxable, they

may be included in the income tests for certain tax offsets.

A useful list of payments made by Centrelink and the Department of Veterans’ Affairs (DVA) is provided in your Tax Rates Handbook, along

with their tax treatment and the item number of the tax return at which they are included, if applicable.

The DVA will issue a PAYG Payment Summary to recipients detailing both the assessable and exempt payments received during the year.

Centrelink no longer automatically issues PAYG Payment Summaries to recipients, however these may be obtained on request.

Alternatively, recipients of both DVA and Centrelink payments will be able to download an income statement by requesting a document

through the relevant page of their myGov account. These details will also be available to be viewed and printed by tax agents from the ATO

Online Services for agents.

This will be the primary source of information regarding these payments, however, some payments will not be shown on the Payment

Summary or ATO Prefill, such as the Pandemic Leave Disaster Payment. These will need to be obtained from other documentation and entered

manually into the tax return.

Normally no tax is deducted from Centrelink or DVA payments, however the recipient can request for this to happen.

Centrelink PAYG Payment

Centrelink PAYG Payment Summaries are issued with all the different payments paid to the taxpayer listed separately.

A typical PAYG Payment Summary will show:

• The type of payment

• The periods paid

• Taxable income

• Tax exempt income (e.g. disability support pension for a person below age-pension age)

• Remote Area Allowance given to supplement the high cost of living in a remote area – not assessable but reduces zone offsets

• Tax withheld

DVA PAYG Payment Summaries will show separately:

• Taxable payments

• Tax withheld

• Tax-free pensions and benefits – this amount is included at Item IT3

• Other exempt payments – this amount is not included on the tax return

• Number of days eligible for Medicare levy exemption

EXEMPT PENSIONS

Exempt Centrelink and DVA payments are not included in assessable income. However, some exempt pensions will be included in the income

test section of the tax return at IT3. These may impact on the calculation of certain offsets. These will be shown on the Centrelink PAYG

Payment Summary as a Tax Exempt payment and on the DVA PAYG Payment Summary as Tax-free pensions and benefits. They will also be

shown as exempt payments on the information which can be downloaded via the ATO Online Services.

Some of the most common pensions included at Item IT3 of the tax return are:

Centrelink Pensions

• Disability support pension (where the recipient is under the age pension age)

• Youth disability supplement where the recipient receives a disability support pension

• Carer payment where both the carer and the care receiver are under pension age or the carer is under pension age and the care receiver

has died.

DVA Pensions

• Pension for defence, peacekeeping or war caused death or incapacity

• Invalidity service pension where the veteran is under the age pension age

• Partner service pension where either

o The partner and the veteran are under the age pension age and the veteran is receiving an invalidity service pension, or

o The partner is under the age-pension age, the veteran has died and was receiving an invalidity service pension at the time of death

• Income support supplement paid on the grounds of invalidity

• Veteran payment under an instrument made under Part IIIAA of the Veteran’s Entitlements Act 1986

• Defence Force income support allowance paid when receiving an exempt social security pension or benefit.

• Certain payments under the Military Rehabilitation and Compensation Act 2004.

52

OTHER EXEMPT INCOME FROM CENTRELINK

Centrelink payments such as a bereavement payment, rent assistance and carer allowance are also exempt. However, these amounts are

not required to be included in the income test section of the tax return. They will generally not appear on the PAYG Payment Summary or

on the income information available to be downloaded from the ATO Online Services into the tax return. These amounts may be taken into

consideration when calculating a carried forward tax loss.

AUSTRALIAN DISASTER RECOVERY PAYMENT

This payment provides $1000 per eligible adult and $400 per eligible child for people who have lost their homes or whose homes or major

assets have been directly damaged or who are the immediate family members of a person who had died as a direct result of a natural disaster.

These payments are exempt income. They are not included in the tax return, either as assessable income or at Item IT3, however they will be

applied to reduce tax losses from an earlier year.

NON-ASSESSABLE NON-EXEMPT PAYMENTS FROM CENTRELINK

Some payments from Centrelink are classed as non-assessable non-exempt income. These amounts are not included in assessable income

and not included in the income test section of the tax return. They will not be taken into consideration when calculating a carried forward tax

loss. In particular, the COVID 19 Disaster Payment is non-assessable non-exempt income.

COVID-19 DISASTER PAYMENT

A payment is available for each period of lockdown for eligible workers in all Australian states who are unable to work and earn income as a

result of a state lockdown of 7 or more days.

This payment is not available for workers in receipt of any of the following payments:

• Income support payments

• Pandemic leave disaster payment

• Business support payments

In addition, workers must have used up other pandemic state based entitlements and all leave entitlements, except annual leave, and have

liquid assets of $10,000 or less.

Due to a change in legislation, the COVID-19 Disaster Payment was reclassified from assessable income to non-assessable non-exempt

income after the end of the 2021 financial year. This change was backdated, so taxpayers who received the payment in the 2021 year and

included the amount in assessable income can amend their tax return to exclude the amount.

53

DISASTER RECOVERY ALLOWANCE FOR 2019-20 BUSHFIRES

The disaster recovery allowance provides income support to employees, primary producers and sole traders who can demonstrate they have

experienced loss of income as a result of a natural disaster. Although the disaster recovery allowance and the disaster income support allowance for special category visa (subclass 444) holders are both generally assessable income, payments in relation to the 2019-20 bushfires

have been made non-assessable non-exempt income and will not be required to be included on the tax return, either as assessable income or

as exempt pension payments.

Reference Point

For more details on assessable and exempt Centrelink payments, refer to the ATO website. Click here to access this page. For information on

disaster assistance payments click here

AMENDED STATEMENT

Sometimes a client will receive an AMENDED statement from Centrelink and it is important to read it carefully to determine what details have

been changed.

Amended details will not be reflected in the information available from the ATO Online Services. The details must be taken from the paper copy

issued by Centrelink.

Where a taxpayer has been asked to repay an amount received from Centrelink that has been included in their taxable income in a previous

year, they may be able to request an amendment to their tax assessment for the relevant year, if the reduction in Centrelink income will result

in a lower tax liability. Once they have either repaid the amount or entered into an arrangement to repay the amount, they should request an

amended PAYG Payment Summary to reflect the updated information.

Although there is technically no time limit on requesting an amendment to a tax return due to the requirement to repay income that has

previously been included as assessable income, where amendments are lodged electronically outside the 2 year amendment period, the ATO

will generally automatically reject the request. An objection should be lodged.

ITEM 1 – PARENTAL LEAVE PAY AND DAD AND PARTNER PAY

PARENTAL LEAVE PAY (PLP)

The paid parental leave scheme provides eligible working parents with up to 18 weeks of government–funded income equivalent to the

national minimum wage (increasing to 20 weeks for a child born or adopted form 1 July 2023). Participation in the paid parental leave scheme

is optional.

Parental Leave Pay can be split and be taken over 2 periods within 2 years and can be claimed for 1 set period and 1 flexible period.

To be eligible, the primary carer must have been in paid work and have been engaged in employment continuously for at least 10 of the 13

months prior to the birth or adoption of the child (there are some exceptions). They must also have undertaken at least 330 hours of paid work

during the ten-month period. There were some exemptions from the work test during COVID. An income test of $168,865 (for the 2023 year)

applies.

For a child born or adopted from 1 July 2023, if the applicant does not meet the income test, they can still be entitled to paid parental leave if

the total of their adjusted taxable income and their partner’s adjusted taxable income (if applicable) is up to $350,000.

PLP is available to employees, including casual employees, contractors and the self-employed.

Should the primary carer return to work before the payment ceases, the balance of the payment can be transferred from the primary carer to

another carer.

PLP is taxable income and will affect entitlement to family assistance payments, income support payments and child support payments.

Whether it is paid by the taxpayer’s employer or Centrelink, tax will be withheld from each payment. If paid by the employer, the amounts will be

included in the Total Gross Amount / Gross Payments on the Income Statement from the employer.

As these payments represent employment income (rather than a benefit), they must be reported at Item 1 on the tax return, even if they have

been paid directly from Centrelink.

Superannuation Guarantee payments are not required for PLP.

56

DAD AND PARTNER PAY

Dad and Partner Pay supports dads or partners caring for a child born or adopted before 1 July 2023 with up to two weeks’ governmentfunded pay if they are on unpaid leave from work or are not working. (From 1 July 2023, Dad and partner pay has been combined with Parental

Leave Scheme, allowing both parents to share the 20 weeks Paid Parental Leave.)

Dad and Partner Pay cannot be transferred to another person.

Dad and partner pay is included at Item 1 of the Income Tax Return.

ITEM 5 – GOVERNMENT PAYMENTS

The following Commonwealth of Australia government allowances and payments are included at Item 5 of the Income Tax Return:

• Jobseeker payment

• Youth allowance

• Austudy payment

• Parenting payment (partnered)

• Partner allowance

• Special benefit

• Widow allowance

• Farm household allowance

• Education payments of any of the following for taxpayers 16 years of age or older

o ABSTUDY living allowance

o Payments under the Veterans’ Children Education Scheme

o Payment under the Military Rehabilitation and Compensation Act Education and Training Scheme 2004 – shown as ‘MRCA

Education Allowance’ on the PAYG Payment Summary – individual non-business

• Other taxable Commonwealth education or training payments shown on the PAYG Payment Summary

• Youth disability supplement as a component of

o Youth allowance

o ABSTUDY living allowance

• A Community Development Employment Project (CDEP) scheme participant supplement paid by Centrelink

• Disaster recovery allowance (DRA) (but not in relation to 2019-20 bushfires)

• Disaster income support allowance for special category visa (subclass 444) holders (but not in relation to 2019-20 bushfires)

57

In addition, the following amount paid by an employer is shown at Item 5:

• An income support component from a Community Development Employment Project (CDEP) – shown as ‘Community Development

Employment Projects (CDEP) payments’ on an Income Statement or PAYG Payment Summary – individual non-business

ITEM 6 – TAXABLE GOVERNMENT PENSIONS & ALLOWANCES

Commonwealth of Australia government pensions and allowances which are included at Item 6 of the tax return include:

• Age pension

• Bereavement allowance (closed to new claims 20 March 2020)

• Carer payment (carer or care receiver over pension age)

• Disability support pension where the taxpayer has reached pension age

• Education entry payment

• Parenting payment (single)

• Age service pension

• Income support supplement

• Defence Force Income Support Allowance (DFISA) where the pension, payment or allowance to which it relates is taxable

• DFISA-like payment from the Department of Veterans’ Affairs (DVA)

• Veteran payment

• Invalidity service pension where the taxpayer has reached age pension age

• Partner service pension

ITEM 24 – OTHER INCOME

Taxable allowances or payments received from Services Australia that have not been shown at Items 1, 5 or 6, are included at Item 24

Category 4 of the tax return. This includes:

• Pandemic leave disaster payment

• High risk settings pandemic payment

• Farm financial assessment supplement

• Farm household allowance supplement

• Farm household allowance relief payment

• Activity supplement (payable to recipients for Farm household allowance for activities that relate to training or study to assist with farm

management and professional advice)

• COVID-19 test isolation payments

• Disaster recovery allowance top-up

58

PANDEMIC LEAVE DISASTER PAYMENT

A one-off payment to eligible workers in all Australian states. The payment assists eligible individuals who are unable to work and earn income

while under a direction to self-isolate, quarantine or who are caring for someone who has tested positive for COVID-19.

This payment is not available for workers who are already receiving another form of income or government assistance.

This payment ceased on 14 October 2022.

HIGH RISK SETTINGS PANDEMIC PAYMENT

High-Risk Settings Pandemic Payment (HRSPP) is a lump sum payment to assist people during the time they can’t work and earn an income

because they have tested positive for COVID-19. To be eligible, recipients must meet all of the following:

· not have claimed or been paid HRSPP or Pandemic Leave Disaster Payment for any day since testing positive to COVID-19

· work in a high-risk setting (aged care, disability care, Aboriginal health care or hospital care. For claims submitted from 11 November 2022,

a high-risk setting also includes custodial facilities, such as prison, youth justice and secure welfare services)

· have no paid leave entitlements available

· have lost at least 8 hours or a full day’s work

· have liquid assets of less than $10,000 on the first day of the period they are claiming for

· have not exceeded the claiming limit

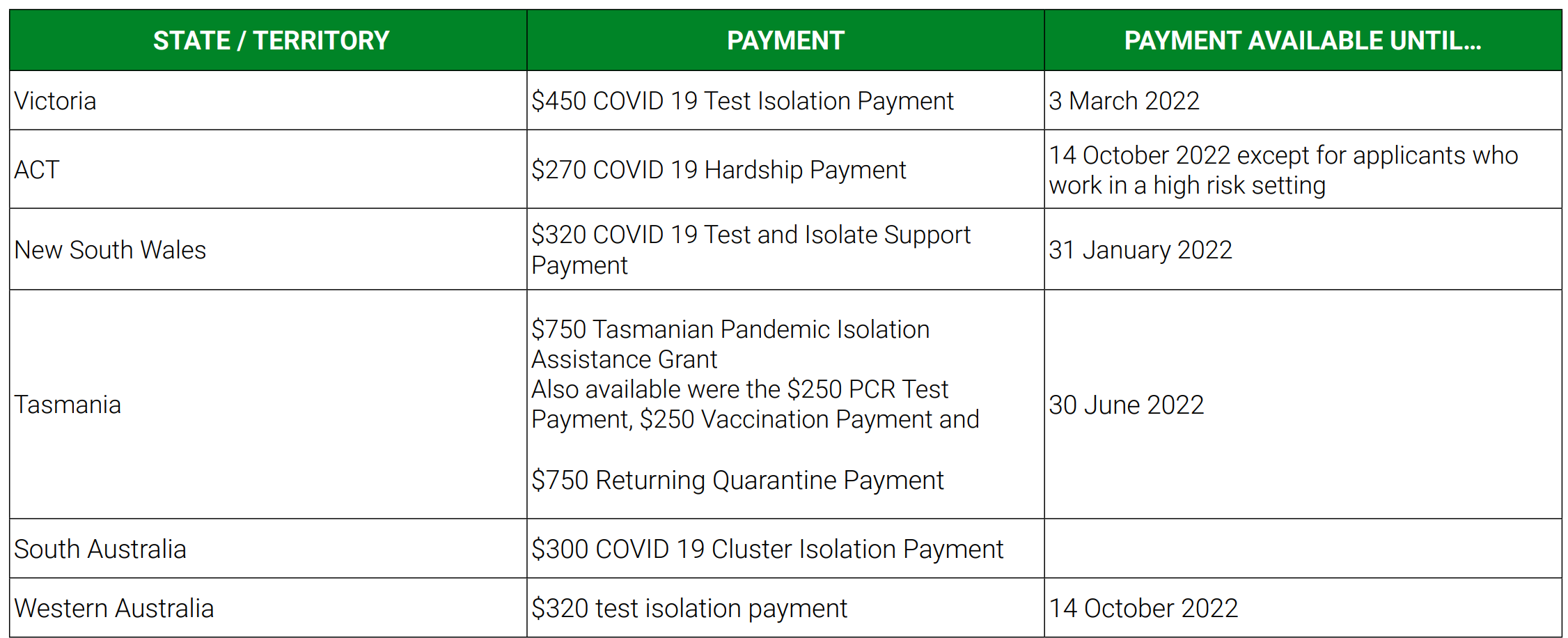

COVID-19 TEST ISOLATION PAYMENTS

Most states and Territories provided financial support, in the form of a one-off payment, for workers if they were required to self-isolate to wait

for the results of a coronavirus test. These payments are assessable income. In most cases they were not available to recipients of the $1,500

pandemic leave disaster payment.