Item D5 – Other work-related expenses

The types of deductions an employee may be able to claim will depend on their occupation.

When determining whether an amount is deductible in a specific case, remember the rules that must be satisfied.

Where an expense is incurred on an item that is used partly for income producing purposes and partly for private purposes, only the taxable

use percentage is deductible.

Is the expense an allowable deduction?

The answers to the following must be YES

• Has the expense been incurred?

• Was it incidental to and had a direct relationship to the occupation?

• Can the claim be substantiated?

The answers to the following must be NO

• Was it capital?

• Was it private or domestic in nature?

• Did it produce exempt or non-assessable income?

• Was the expense incurred at a point too soon?

• Is there a specific provision of the ITAA which prevents it from being deductible?

Where the items are capital in nature, an immediate deduction will not be allowed, however a deduction for the taxable use percentage of

the decline in value may be claimed. This will be covered in a later module.

The following is a list expenses that may be incurred by employees, and whether they may be deductible or not. This list is not exhaustive. It

is designed to be used as a reference and to assist you in applying the general rules of deductibility. However, you will need to be very familiar with the common expenses. Common expenses will be featured in the homework and quizzes.

Most of these expenses are claimed at Item D5, where they are incurred for work related purposes. If the expenses relate to a claim for a deduction for self-education expenses (covered in detail in a later module) they will be claimed at Item D4. Where they are claimed at another

item this is mentioned.

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

25

COMMON DEDUCTIONS

Advertising Expenses

These may be allowable for occupations such as commission-based real estate agents.

Annual Practising Certificates, Registrations, Accreditations

A deduction can be claimed for the cost of renewing an annual practising certificate, membership or accreditation if it is required to work

in the current field of employment. This can include trade licences for plumbers, electricians and carpenters, crane, hoist and scaffolding

licences for construction workers, responsible service of alcohol and gaming licences for hospitality workers and registrations for nurses,

doctors, teachers and other professionals.

However, if a practising certificate, professional registration or accreditation is required before commencement of work in the field, the initial

cost is not deductible. This is because the expense is incurred to enable the taxpayer to start employment in the field, not during the course

of earning income.

Bank Fees

A deduction is not allowed for account keeping fees or overdraft fees as a work-related expense, as these are not incurred in earning

employment income. A deduction can be claimed for transaction fees charged when making a work-related purchase.

Books, Technical Journals, Digital Information Services

Where the content of books, periodicals or technical journals is sufficiently connected to employment income, a deduction can be claimed

for these expenses. Where the content is too general in nature and does not specifically relate to the current income producing activity, no

deduction will be allowed.

Briefcases, Bags And Cases for Work Items

A deduction is allowed where the item is used for transporting work-related files and equipment such as laptops and tablets. A deduction

may also be claimed for duffel bags, backpacks and handbags used for the same purpose. If the items are used for transporting personal

items as well, apportionment may be required.

No deduction can be claimed if the briefcase or bag is used only for personal purposes such as carrying lunch and beauty or hygiene

products; this is private use.

Calculators & Electronic Organisers

A deduction is allowed for the taxable use percentage.

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

26

Cash Shortages

A taxpayer who is in a position of handling money and is required to make up a shortfall or deficiency will be allowed a deduction for the full

amount of the cash shortage. A diary entry in support of the claim must be held.

Childcare Expenses

A deduction is not allowed.

Clothing

See Item D3.

Club Membership Fees

A deduction is generally not allowed for the cost of Club Membership fees, regardless of the business use made of the club by the member.

These are regarded as entertainment. There are some exceptions:

• The cost of Airport Lounge Membership is deductible where the facilities are used for work related travel. Although the clubs also

provide some food, drink and recreation, they also provide business facilities and services related to the travel of their members. As

such, the membership is not considered entertainment.

• Membership fees paid by police officers to Australian Federal Police pistol clubs are deductible to the extent they are incurred for work

related purposes.

Coaching Classes

A deduction is allowed for performing artists in maintaining skills.

Commissions

A commission paid to an agency for work gained through the agency is deductible.

Computers, Laptops and Other Devices and Software

The cost of buying and using a computer or similar device is often an integral part of self-education or work deductions. The original cost

of the computer will be depreciated. The cost of memory sticks, USB drives, apps, paper, printer cartridges, repairs etc. can also be claimed.

Computer software (but not software subscriptions) is depreciated if the cost is more than $300.

Where a computer is used for partly work-related purposes and partly for private purposes, a diary record should be kept for four weeks to

establish the taxable use percentage.

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

27

Conferences, Seminars, Training Courses and Workshops

A deduction is allowed for the cost of attending conferences, seminars, training courses and workshops if they are directly related to the

field of employment. The cost of the conference or seminar is claimed at Item D5. Any related accommodation and travel (by plane or bus)

is claimed at Item D2. Travel (by car) will be claimed at Item D1. Motor vehicle and other travel claims are discussed in more detail in a later

module.

Where the expenses relate to a course of education provided by a school, college, university or other place of education and undertaken to

gain a qualification, the deduction for all expenses, including travel, is claimed at Item D4. Self-education is covered in detail in a later

module.

Apportioning claims

Where travel is undertaken for a study tour or attendance at a work-related conference or seminar and also for private purposes, it may be

necessary to apportion the expenses.

When determining whether it is necessary to apportion the expenses, consideration must be given to the dominant purpose of the travel. If

the private purpose is merely incidental to the main income-earning purpose, apportionment is not appropriate TR 2023/D1. Where the

dominant purpose of the travel is private in nature, and the attendance at a seminar is merely incidental, only expenses that related directly

to the seminar can be claimed. In other circumstances, it may be necessary to apportion travel expenses on a reasonable basis.

Example

Gerard, a qualified architect, attends an eight-day work-related conference in Hawaii on trends in modern architecture. One day of the

conference involves a sightseeing tour of the island and a game of golf is held on the final afternoon of the conference. As the main purpose

of attending the conference is the gaining or producing of income, the total cost of the conference (airfares, accommodation and meals) is

allowable.

The existence of private pursuits, such as the island tour and the game of golf, is purely incidental to the main purpose and does not affect

the characterisation of the conference expenses as wholly incurred in gaining assessable income.

Example

Linda, a doctor, was holidaying in Cairns when she became aware of a work-related seminar on the current treatment of cancer patients.

The cost of the half-day seminar was $200. Linda is able to claim a deduction for the cost of the seminar because it is directly attributable to

an income-earning purpose. However, no part of her airfare to Cairns or her holiday accommodation is an allowable deduction.

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

28

Example

Lincoln flies to London for a 10-day international, work-related conference. Lincoln stays over for an extra four days to do some sightseeing.

As the sightseeing is not an incidental part of the conference or the trip as a whole, Lincoln can only claim the work related portion of the

airfares (10 days / 14 days) and the accommodation and meals for the 10 days he attends the conference.

Covid-19 Testing Expenses

A deduction can be claimed for COVID-19 tests that were used by an employee to determine whether they could attend or remain at work.

This includes polymerase chain reaction (PCR) tests through a private clinic or tests listed in the Australian Register of therapeutic Goods,

including rapid antigen test (RAT) kits.

Dry Cleaning

A deduction is allowed if the clothing is of a type that would be an allowable work-related deduction.

Education Expenses

A deduction is allowed for self-education expenses where the expenses have the necessary connection with the production of the taxpayer’s

assessable income. Where the expenses relate to a course of education provided by a school, college, university or other place of education

and undertaken to gain a qualification, the deduction is claimed at Item D4. A claim can be made for seminars and refresher courses at Item

D5. Self-education is covered in detail in a later module.

Electricity

See Working from Home Expenses

Employment Agreement

Costs associated with extending, varying, renegotiating or renewing an employment agreement or drawing up a replacement employment

agreement with an existing employer are deductible if the agreement allowed for such changes (TR 2000/5).

Expenses incurred in applying for a promotion are deductible, provided they are likely to lead to an increase in the taxpayer’s assessable income, without a change in their income earning activity.

Entertainment

Generally, no deduction is allowed for entertainment expenses. This restriction extends to entertainment in the form of food, drink or recreation.

Where an employee, who is travelling overnight in the course of performing employment duties, consumes food and drink, the food and

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

29

drink is generally not regarded as entertainment, so will be deductible (discussed in a later module). However, expenses such as ‘business

lunches’ with clients and staff social functions will generally be classed as entertainment and not tax deductible.

Although most of the ATO rulings on entertainment are in relation to business expenses and FBT, the same principles may be applied to

employees. In determining whether an expense is deductible we need to look firstly at whether there is sufficient nexus between the

expense and earning assessable income, or whether the link is too tenuous, and then at whether the expense is specifically disallowed as it

is entertainment.

To determine whether an expense of food and drink is entertainment, you need to consider:

• Why it is being provided – When provided for the purpose of refreshment it will not generally be considered entertainment. When

provided in a social situation, it will generally be considered entertainment.

• What is being provided – the more elaborate the meal, the more likely it is to be entertainment.

• When it is being provided – Food and drink provided in work hours is less likely to be considered entertainment.

• Where it is being provided – Food and drink at a business premises is less likely to be considered entertainment than food and drink

provided at a restaurant or café.

Examples of expenses that are not considered entertainment, so are deductible:

• The cost of attending a social function by a journalist required to report on the function (TR 98/14).

• Meals of a restaurant reviewer or tickets of a theatre critic.

Examples of expenses that are not deductible:

• Wine purchased by a food and beverage analyst for tasting at home (ATO ID 2002/319).

• Meals purchased by chef at other restaurants in order to keep up with food trends.

In both of the above, the expense is not incurred in order to earn the income – the link is too tenuous to allow a deduction.

Fines

A deduction is not allowed where imposed under Australian or foreign law.

First Aid Courses

A deduction is allowed where the taxpayer is a designated first aid person, and they are required to undertake first aid training to assist in

emergency work situations.

Fitness Expenses

Fitness expenses are generally considered a private expense and a deduction is not allowable. This is the case even for occupations that

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

30

may require the taxpayer to remain physically fit, or to pass medical examinations and fitness tests to maintain employment, such as police

officers and other emergency personnel, defence force personnel, fitness instructors and performing artists.

However, a deduction is allowable if the taxpayer can demonstrate that strenuous physical activity is an essential and regular element of

their income earning activities and that costs were incurred to maintain a level of fitness WELL ABOVE the general occupational standard.

It is considered a police academy or defence force physical training instructor may be in this category. Other occupations may include

professional sportspeople, trapeze artists or tumblers working in a circus, and those in tactical response units, specialist search and rescue

teams or special combat squads.

Expenses that may be claimed in the above circumstances include gym fees and depreciation of gym equipment. No deduction is available

in respect of expenditure on any items of conventional clothing which may be used in the course of keeping fit. This would include such

things as tracksuits, running/aerobic shoes, socks, T-shirts or shorts.

The following expenses are not allowable health and fitness deductions:

• the cost of a program specifically designed to manage weight

• the cost of normal food substitutes or the cost of food for special dietary purposes

• the cost of vitamins, minerals, or sports supplements, such as protein shakes.

Gifts

Real estate industry employees who earn commission income are allowed a deduction for the cost of gifts and greeting cards bought for

clients. No deduction is allowable for these expenses where the employee is not paid on commission, as the connection to such expenditure

and increased income is remote.

For employee teachers, no deduction is allowed for expenditure on items supplied to students for their own individual needs, such as books

and uniforms, Christmas gifts, or replacing money lost by students. However, a deduction will be allowed where the items are teaching aids

or teaching rewards.

Glasses and Contact Lenses

A deduction cannot generally be claimed for the cost of prescription glasses or contact lenses. However, a deduction can be claimed for

safety glasses, sunglasses or anti-glare glasses (including prescription sunglasses and prescription safety glasses) when required for

work-related purposes. Glasses are also allowed where they form part of a stage costume.

Grooming

A deduction is generally not allowable for grooming expenses (cosmetics and hairdressing, razor blades and electric shavers) even when an

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

31

employee may be required to maintain a high standard of appearance. Not even defence force personnel are allowed a deduction for

haircuts to comply with military regulations. Similarly, police officers and fire brigade officers are not allowed a deduction for haircuts.

A deduction is allowable for performing artists for the cost of stage makeup and for the cost maintaining a particular style or length of hair

for a performance.

A deduction is allowed for rehydrating moisturiser and hair conditioners for flight attendants, due to the drying effects of the harsh working

conditions. Moisturisers and conditioners may also be deductible to a hydrotherapy assistant who is constantly exposed to chlorinated

water (TR 2003/16).

For sun protective cosmetics see Sun Protection.

Home Office Expenses

See WORKING FROM HOME EXPENSES

Insurance

Policies that insure tools and equipment are deductible to the extent that the items are used for work.

The cost of professional indemnity insurance for work related purposes is also deductible.

Travel insurance is not deductible even if the related travel is deductible. Travel insurance policies cover private items such as illness, loss of

luggage and theft.

The deductibility of Income Protection and Sickness and Accident policies as well as vehicle insurance will be discussed later in the course.

Interest

Interest on a loan taken out to purchase work equipment or for other work-related expenses may be claimed to the extent of the taxable use

percentage. This is common for the purchase of cars, tools and computers.

Internet

A deduction is allowed for work related percentage of internet use. A reasonable basis to work out work related use could include:

• the amount of data downloaded for work as a percentage of the total data downloaded by all members of the household

• any additional costs incurred as a result of the work-related use – for example, if the work-related use results in exceeding the monthly

cap

• the time spent by the taxpayer using the internet for work purposes compared to time spent by all occupants using the internet for

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

32

private purposes

If using the amount of data downloaded or the time spent using the internet, a diary of work use and private use must be kept over a

representative 4-week period to establish the work use percentage. This percentage can then be applied to the costs incurred for the full

year.

Remember if it is a home internet plan and other people in the household are using the internet, their usage must also be taken into

consideration.

For bundled internet and phone plans, see TELEPHONE.

Where the internet expense claim is made as a consequence of working from home, a set rate may be able to be claimed, which will take

into consideration expenses incurred such as energy, mobile and home phone, internet, computer supplies and stationery (see Working from

Home), rather than calculating these items separately. The method used to claim should be the one that gives the highest claim, provided

the necessary records are available.

Laundry

See Item D3 above.

Legal Expenses

To be deductible, legal expenses must be incurred in deriving assessable income and cannot be private, domestic or capital in nature. Legal

expenses are considered capital in nature if the benefit being sought is capital in nature. The success or failure of the legal action has no

bearing on whether or not the expenses are deductible.

Examples of deductible legal expenses include those incurred:

• in recovering a payment in lieu of a termination notice period

• in recovering unused annual leave and unused long service leave on termination

• by an employee in recovering wages paid by a dishonoured cheque

• by an employee to prevent defamatory statements being made by a colleague

• in pursuing an assessable workers compensation claim or income entitlements under an employment agreement

Examples of legal expenses that would generally be non-deductible include:

• legal expenses incurred by an employee in pursuing compensation from an employer in the nature of a golden handshake or damages

relating to a wrongful dismissal. These amounts, although assessable income, are capital in nature, therefore the legal expenses are

capital in nature.

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

33

Other legal expenses, such as borrowing expenses, mortgage discharge expenses and expenses involved in preparation of leases are deductible under specific sections of the ITAA when they are incurred in respect of the derivation of assessable income. These are covered in a

later module.

Licences, Permits and Cards

A deduction is not allowed for the cost of acquiring or renewing a driver’s licence. This is a private expense even if driving is an essential part

of the employment activity and a having a licence is a condition of employment.

A deduction can be claimed for additional costs incurred to obtain or renew a special licence or condition on a licence in order to perform

current employment duties, or for any regulatory permits, certificates or ‘cards’ that relate to employment.

Examples include:

• Dangerous goods licence

• Forklift licence

• White card

• Working at heights ticket

If a taxpayer is required to have a particular licence, permit or card before they can be employed in an occupation, the initial cost of obtaining

it is not deductible.

Lunch Boxes, Travel Mugs, Coolers Etc

No deduction is allowed for items you use to take your food or drink to work or use at work. These are private expenses.

Meals

No deduction is allowed for the cost of meals during the normal working day. The cost of meals may be claimed where the taxpayer has

travelled away overnight for work (covered in a later module). The cost of meals may also be claimed where an award overtime meal allowance has been received (see Overtime Meals below).

Medical Examinations

A deduction is allowed for the cost of medical examinations required for licence renewals (where the cost of the licence renewal is allowable) as well as the travel to the examination.

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

34

Medical Expenses

Medical expenses are generally not deductible. Common examples of non-deductible medical expenses are most immunisations,

prescription glasses (unless prescription sunglasses or prescription safety glasses), contact lenses (unless tinted for performing artist),

hearing aids and stress management. No deduction is allowed for contributions to a private health fund, even if it is a condition of

employment.

Newspapers And Other News Services And Subscriptions

The cost of newspapers, news services and other news subscriptions is generally considered private in nature. The benefits of staying

informed on news matters will usually be no more than incidental to employment duties and the expense too remote from income earning

activities to be deductible.

A deduction is allowed if it can be shown there is sufficient connection between employment duties and the specific publication. The

expense will need to be apportioned if the publication is used for private purposes as well.

Overtime Meals

Generally, an employee cannot claim a deduction for the cost of meals consumed at work, as these expenses are considered private in

nature. However, a deduction may be allowed for the cost of meals purchased and consumed when working overtime. In order to be able to

claim a deduction for overtime meals, the employee must have received a bona fide overtime meal allowance under an industrial law, award

or agreement and this allowance must be included as assessable income.

A bona fide overtime meal allowance is an amount that could reasonably be expected to cover the costs of food and drink in connection

with overtime. A token amount (i.e. a minimal amount paid without regard to likely expenses) is not a bona fide meal allowance.

Meal Allowances – STP Reporting

Under STP guidelines, a meal allowance refers to an allowance defined in an industrial instrument that is paid to compensate the employee

for meals consumed during meal breaks connected with overtime worked, so is consistent with the definition of deductible overtime meals.

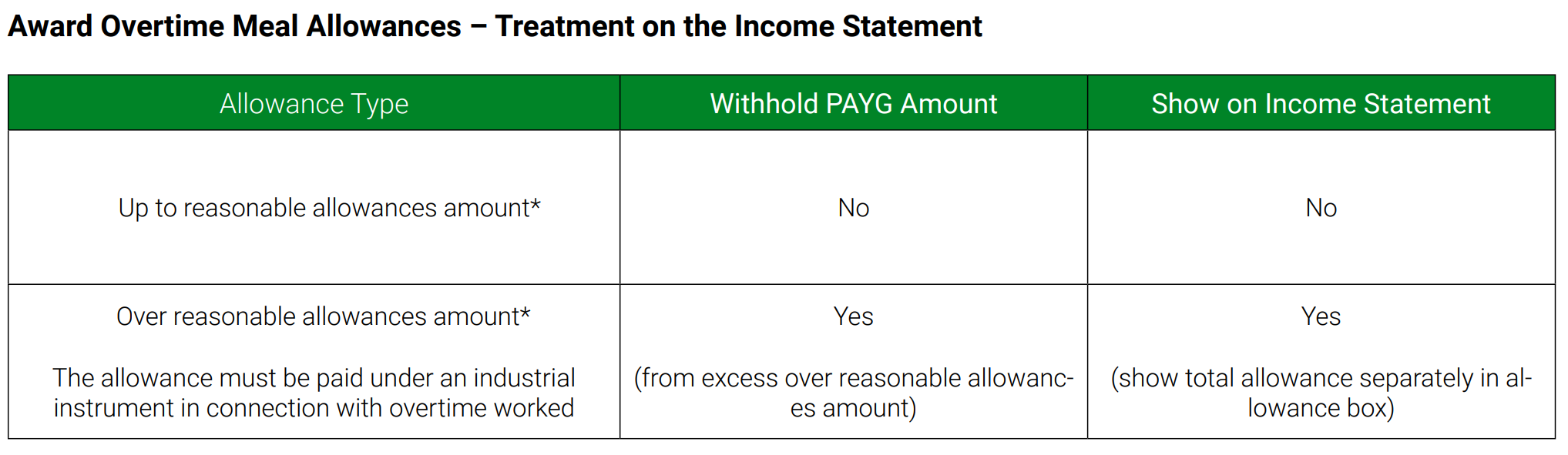

Where an overtime meal allowance has been paid up to the reasonable amount set by the Commissioner, employers are not required to

deduct a withholding amount (Taxation Administration Act 1953 – PAYG Withholding Variation: Allowances – Legislative Instrument Issued

17 June 2015), nor are they required to include this amount on the Income Statement, either as an allowance or as part of the gross

payment.

Employers are only required to include an amount paid as an overtime meal allowance on the income statement if the amount exceeds the

ATO reasonable amount.

Other allowances relating to meals, such allowances paid to compensate the employee for the cost of meals purchased during ordinary

work hours (including night shifts) or allowances paid to compensate the employee for working through their meal break should be shown

under the category ‘other’ allowances. No deduction is allowed for the cost incurred on meals that relate to these allowances. An allowance

to compensate the employee for the cost of meals while travelling away from home overnight is shown as a travel allowance (deductions

for these expenses are covered in a later module).

The reporting guidelines for employers have changed over the years, and some employers will still include allowances that should be classified as other allowances on the income statement as a meal allowance or may include overtime meal allowances that are below the reasonable allowance on the income statement.

If an allowance has been included on the income statement, it must be included at Item 2 of the tax return as assessable income. Where a

meal allowance has been included on the income statement, the true nature of the allowance should be established.

If the amount is a bona fide overtime meal allowance, the employee may be able to claim a deduction for the amount they have spent on

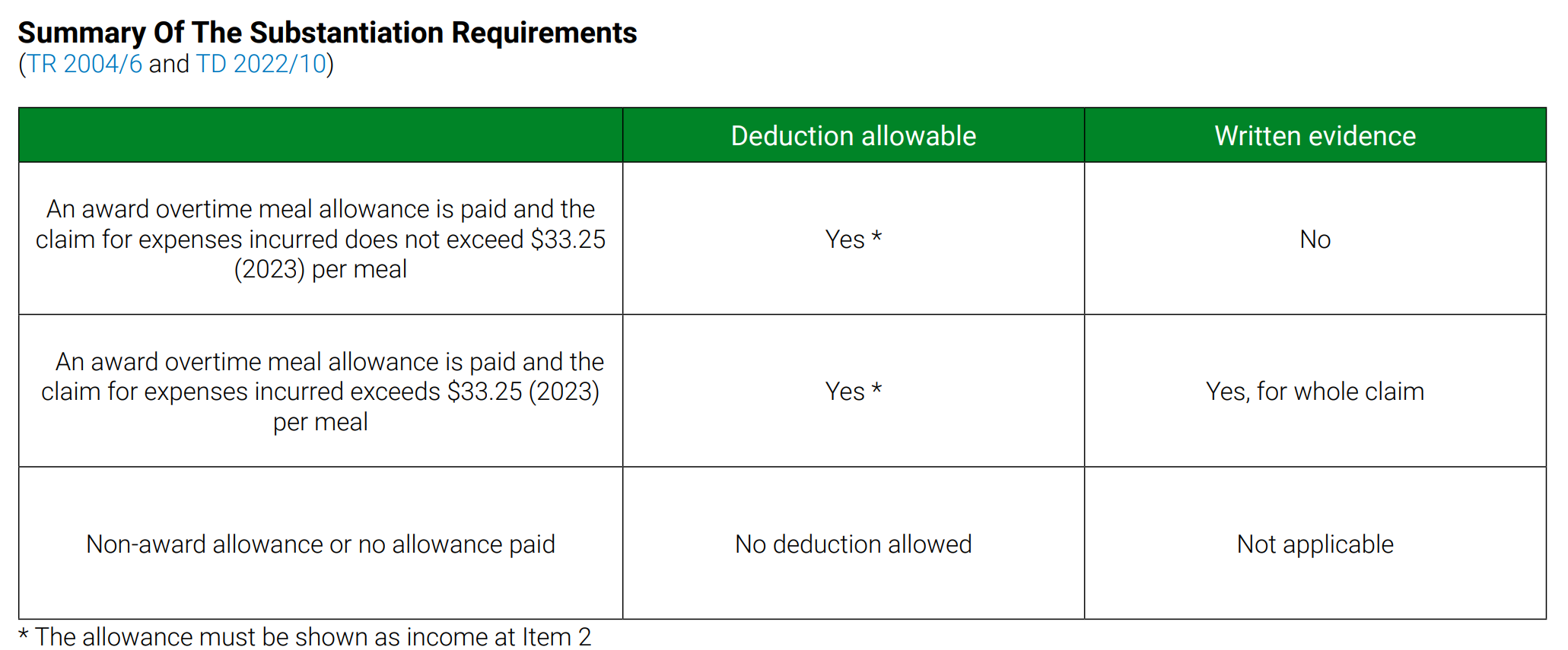

meals when working overtime.

Where the claim for the cost overtime meals does not exceed the reasonable amount allowed by the Commissioner, written evidence is not

required. The reasonable amount is set by the Commissioner each year and for the 2023 year is $33.25 per meal (TD 2022/10). However, if

audited, taxpayers will need to be able to explain how the claim was calculated. It would be advisable to keep a sample of receipts or other

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

36

documents to show the amount actually spent.

A deduction of the reasonable amount per meal is not automatically allowable. It is required that the taxpayer must have incurred the

expense and only the amount incurred can be claimed.

Where the employee is claiming a deduction for an amount over the reasonable allowance, the full amount must be substantiated, not just

the amount above the reasonable allowance. Receipts must be kept for the full year. If receipts for the full amount are not available, the

claim will be limited to the total of the available receipts or the amount calculated under the reasonable allowance provisions, whichever is

the greater.

Meal Allowance included in the gross salary on the Income Statement

An amount for overtime meals that has been folded in as part of normal salary or wages income is not considered to be an overtime meal

allowance. This type of allowance will be included in the gross salary that is reported on the Income Statement or PAYG Payment

Summary. The ATO generally takes the view that the amount is not an allowance as it becomes part of the employee’s salary and is paid

whether or not overtime is worked. For example, an employee may receive a regular payment of $10 per day for overtime meals, irrespective

of whether they have worked overtime.

However, where an employer has incorrectly included an overtime meal allowance as part of the gross salary on the Income Statement or

PAYG Payment Summary, a deduction may be claimed for the expenses incurred on meals when working overtime, subject to the above

rules. In these circumstances, the employee should obtain a letter from the employer that provides details of the allowance paid and confirms the payroll error made. Careful examination of the final payslip and Income Statement or PAYG Payment Summary will establish

whether an overtime meal allowance has been included with the gross salary amount.

The details on the Income Statement should be reported on the tax return exactly as they are shown on the Income Statement – that is the

gross amount from the income statement, including the overtime meal allowance, should be included at Item 1. A copy of the final payslip,

showing the year-to-date figures and confirming that a genuine overtime meal allowance has been included in the gross should be kept.

Claiming a Deduction for Overtime Meals not Included on Income Statement

Where an overtime meal allowance has been received but is not shown on the Income Statement (as it is below the reasonable allowance)

the allowance is not required to be shown as assessable income in the employee’s tax return, provided the allowance has been fully

expended on deductible expenses. If the allowance is not shown as income, no deduction can be claimed for the expense incurred.(TR

2004/6)

However, an allowance received by an employee is still assessable income (s 15-2 ITAA 1997). An employee may choose to include the allowance at Item 2 of the tax return, even if it has not been shown on the Income Statement. If they do so, they will be able to claim a deduc-

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

37

tion for the expenditure on overtime meals, provided the other requirements are satisfied. If audited, the employee will need to be able to

show that an overtime meal allowance has been received. A copy of payslips showing the amount that has been paid or a letter from the

employer should be retained with their tax records.

Example

Sally worked overtime five times during the year and was paid an award meal allowance of $22 each time. She spent $19 per meal. $110 is

shown under Meal Allowance on her Income Statement, so she will need to declare that amount at Item 2 on the tax return. She can claim

$95 ($19 x 5) at Item D5. Her deduction is less than the reasonable amount and so she is not required to substantiate her claim.

If Sally’s employer had not included the meal allowance on her Income Statement, she would not be required to include the amount as assessable income. If she did not include the amount as assessable income, she would not be entitled to claim a deduction for the amount

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

38

she spent on overtime meals.

Parking Fees

A deduction is allowed while travelling in the course of employment (Module 5). For example, where an employee pays for parking when

attending a seminar or training course, a deduction can be claimed. Where deductible, parking is claimed at Item D2.

No deduction can be claimed for parking expenses incurred when going to the usual workplace. This is a private expense.

Passport

No deduction is allowable for expenses associated with acquiring a passport, as the ATO take the view that a passport relates primarily to

the taxpayer’s right to travel to any overseas destination.

Pay Tv Access and Streaming Services

Generally, the cost of Pay TV access and streaming services are a private expense and not deductible. Even though a taxpayer may be able

to use part of the information obtained in the course of their work, the benefit gained is usually remote and the proportion of the expenses

that relates directly to work is incidental to the private expenditure.

Example

Glenn is a pilot for a domestic airline. He subscribes to a pay television service that has a real-time weather channel. Glenn checks the

weather channel in the morning before flights as he does some preliminary planning for his flights that day. Glenn’s employer also supplies

weather information to him when he arrives at the airport. He is expected to use the information his employer provides in his flight planning.

Glenn can’t claim any part of the cost of his pay television subscription as the benefit he gains from the subscriptions is too remote and the

proportion that relates to his work is incidental.

However, where a taxpayer is required to access Pay TV or streaming services as a direct consequence of their work, they may be able to

claim a proportion of the expense incurred. A reasonable apportionment must be made based on a diary record over a period of time that

reflects a normal usage pattern.

Example

Phil is a sports writer employed by a metropolitan newspaper, who specialises in test cricket and provides coverage for his employer on all

test matches played in the region. Some of the matches Phil is required to cover are only screened on Pay TV and Phil subscribes to a Pay

TV provided in order to compile a report on those test matches. Phil also uses his Pay TV access for private purposes. The work related

proportion of Phil’s monthly access fee is an allowable deduction.

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

39

Police Clearance Certificates

No deduction is allowed prior to commencement of employment. However, ongoing police checks where required for employment are

deductible.

Professional, Business, Trade Associations and Unions

Periodic subscriptions paid by employees to professional, business and trade associations and unions are deductible in full if related to their

employment.

Joining fees are not an allowable deduction. A joining fee is an additional amount levied by some associations on new members. It is

regarded as a once and for all payment which provides the new member with the enduring benefit of membership of the association and as

such is a capital expense (TR 2000/7).

Where a subscription to a professional, business or trade association or union is not deductible under s 8-1, either because it does not relate

to the derivation of assessable income or because it is a joining fee, a deduction will be allowed under s 25-55 of the ITAA 1997. The amount

that is deductible under this section is limited to $42 in respect of each association to which the person belongs in an income year.

If a special levy is imposed by a professional, business or trade association, this will be deductible under s 8-1 if it is to enable the

association to acquire or construct new premises or to refurbish existing premises or to acquire plant and equipment to better enable it to

carry on its activities.

However, the following levies are not allowable deductions under either s 8-1 or s 25-55 of the ITAA 1997:

• payments to, or to assist, a political party

• payments to provide overseas relief

• payments to assist families of employees suffering financial difficulties as a result of employees being on strike or having been laid off

and

• payments by elected trade union official into a general fund for the election of union officials.

Union fees are often deducted from wages and will be shown as a deduction on the Income Statement or PAYG Payment Summary. Care

should be taken to ensure deductions reported on the Income Statement are solely for union dues and deductible levies.

No deduction is allowed for Staff Social Clubs or Staff Association Fees where the funds are used for social purposes.

Protective Equipment / Products

The cost of protective equipment/products is deductible if their use is directly linked to the particular conditions of the taxpayer’s work.

Protective equipment is claimed at Item D5, while protective clothing is claimed at Item D3.

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

40

The taxpayer can claim a deduction for protective equipment such as:

• goggles

• breathing masks

• hard hats and safety helmets

• protective gloves

• safety glasses (including prescription safety glasses)

• sunglasses, where required to work outside (including prescription sunglasses)

• anti-glare glasses (included prescription anti-glare glasses)

• facemasks and face shields

• earplugs

Where a taxpayer is working in a job that requires physical contact or close proximity with customers, clients or work colleagues during

COVID-19, they are able to claim a deduction for face masks, if they have paid for the masks themselves and have not been reimbursed.

Where a taxpayer’s work duties either:

• bring them in close contact with clients or customers or

• involve cleaning a premises,

they will be able to claim a deduction for items such as gloves, sanitisers or anti-bacterial spray.

Removal and Relocation Expenses

A deduction is not allowed for removal and relocation expenses, when either transferring or taking up new appointments. If the employer

pays an allowance to cover an estimate of these expenses, this will be shown on the Income Statement or PAYG Payment Summary as an

allowance. However, no deduction can be claimed for the expense. When the employer reimburses the actual amount of the expense it will

not be required to be shown on the Income Statement. If the employer pays for the expense, it will be exempt from FBT.

Social Functions

A deduction is not allowable for expenditure incurred in attending staff dinners, school formals or similar functions if the cost of the ticket

provides for food, drink or recreation. A deduction is not allowed for the cost of providing morning / afternoon teas or light refreshments for

colleagues. Even if the provision of refreshment is part of ‘team building’, it is not sufficiently connected to the duties by which an employee

produces assessable income and remains a private expense.

Stationery

A deduction can be claimed for the cost of diaries, pens, logbooks or other stationery required for work.

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

41

Sun Protection

A deduction is allowed for the cost of sun protective items for a taxpayer who works for sustained periods outside in the sun, such as landscape gardeners, truck drivers or construction workers.

Allowable expenses include:

• sunscreen lotion

• sunglasses, including prescription sunglasses

• clothing with UV protection

NOTE

Sun hats and other clothing are claimed at D3 – protective clothing.

Cosmetics are usually a private expense and the addition of sun protection does not necessarily make the expense deductible. Where

creams and cosmetics can function both as a sun protection and as a cosmetic, if the primary purpose of the item is for use as a cosmetic

or the product is marketed as a cosmetic, it generally won’t be treated as a sun protective product.

The Department of Health and Therapeutic Goods Administration (TGA) regulates if a product is safe and effective as a sunscreen. Products

regulated as therapeutic goods by the TGA include:

• primary sunscreens (intended primarily for sun protection)

• moisturisers containing sunscreen with Sun Protection Factor (SPF) greater than 15

• sunscreens with ingredients from humans, cows, sheep, goats or mule deer organs

• all sunscreens (with SPF-4 or more) that contain insect repellent.

If a product is safe and effective as a sunscreen, it is given an Australian Register of Therapeutic Goods (ARTG ID) number by the TGA. This

is displayed on the product as an AUSTL number.

The ATO accept any product with an ARTG ID or AUSTL number on the label as a sunscreen rather than a cosmetic. To find out whether a

product has been given an ARTG ID visit the TGA Website.

Example – deduction not allowed for cosmetic containing sunscreen

Jackie is a teacher and has purchased a cosmetic with added sunblock. Once a week, Jackie is required to supervise pupils at their sports

afternoon outdoors. Jackie wears the cosmetic every day and she finds it suitable as a sun protection but it is not a sunscreen approved by

the TGA. As Jackie uses the product primarily as a cosmetic, she will not be entitled to a deduction for the purchase. This is even though she

is exposed to the sun when she is performing her duties on sports afternoon.

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

42

If the product Jackie purchased had been given an ARTG ID by the TGA, she would have to apportion the deduction she claimed for the

product to account for her personal use, which would include the time she does not spend in the sun performing her duties and any other

time she wears the cosmetic outside school hours.

Example – deduction allowed for cosmetic containing sunscreen

Wendy works as a gardener and spends the majority of her working day outdoors. Wendy purchases a tinted moisturiser with a high level

sunblock to use on her face when she is working, along with a sunscreen for her arms and legs. Wendy does not use these products when

she is not working. Wendy checks the TGA website and finds that both the products she uses have an ARTG ID. As Wendy is exposed to the

sun for long periods as a result of performing her duties, the cost of the products is incurred in earning her assessable income. This means

she is entitled to a deduction for the tinted moisturiser and sunscreen she purchases.

Teaching Aids

A deduction is allowable for expenditure incurred on items or teaching aids used in everyday duties of an employee teacher, such as:

• stationery, stamps, stickers, paints, posters, maps, laminating etc.

• books, jigsaws, games, toys

• items used in cooking, sewing or science experiments

• prizes purchased to reward achievement and encourage students

• entrance fees for school excursions

• whistles and stopwatches used by physical education teachers

• cost of maintaining classroom or school pets

Telephones and Other Communication Devices

If the taxpayer uses their own phone in the course of performing their work, they may be able to claim a deduction for the costs incurred if

they paid for these costs and have records to support their claims. If the phone is being used for both work and private use, they will need to

work out the percentage that reasonably relates to the work use.

A deduction can be claimed for the work-related percentage of the following expenses:

• the cost of the phone or device

• related data and internet expenses

• phone or bundle plans.

If the phone or device cost more than $300, the item must be depreciated. Installation and set up costs are not deductible, neither is the

cost of obtaining a silent number.

If the employer provides a phone for work use and is billed for the usage (phone calls, text messages, data) then the taxpayer is not able to

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

43

claim a deduction. Similarly, if any usage is paid for by the employee and is subsequently reimbursed by the employer, no deduction allowed.

Taxpayers who use their phone to seek employment are unable to claim a deduction as they are not yet generating income from the use of

the phone. Similarly, a deduction cannot be claimed by a casual employee where the phone is merely to receive calls from the employer to

ask them to work or for the employee to check on work availability. This cost does not directly relate to the income producing activity – it

simply puts them in a position to earn income.

Incidental use

If work use is incidental and the deduction being claimed is less than $50 in total, a claim can be made based on the following, without

having to analyse any bills:

• $0.25 for work calls made from a landline,

• $0.75 for work calls made from a mobile, and

• $0.10 for text messages sent from a mobile.

These calls and texts should be noted in a diary.

If the deduction being claimed is $50 or more, the claim must be substantiated.

Substantiating a claim

Where the deduction claimed is $50 or more, the taxpayer will need to substantiate the claim with records of the total expense incurred

during the year and records to show how the work related percentage was established. Evidence that the employer expects the employee to

work at home or make some work-related calls will also help to demonstrate that the taxpayer is entitled to a deduction.

How to apportion the work use of a phone

To establish the work related percentage of a phone or device, a record of the device usage should be kept over a 4-week representative

period in each income year, showing work related and private use. This percentage can then be applied to the expenses incurred in the full

year. These records may include diary entries, electronic records and bills. There are many different types of plans available so care will need

to be taken to determine the work use on a reasonable basis.

If the taxpayer has a phone plan where they receive an itemised bill, they may be able to establish the percentage of work use from the

itemised account. Where an itemised account is not received, a diary record of the device usage will need to be kept over a representative

4-week period to establish the work related percentage.

The percentage needs to be worked out using a reasonable basis. This could include:

• the number of work calls made as a percentage of total calls

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

44

• the amount of time spent on work calls as a percentage of total calls

• the time used in different functions for work purposes compared to private purposes – for example, some taxpayers may use the

camera and gaming applications exclusively for private use whereas other taxpayers may require the camera and many applications for

work purposes

• the amount of data downloaded for work purposes as a percentage of total downloads

The type of use of the phone or device will be important. For example, if the taxpayer predominantly uses a mobile phone for phone calls,

then analysis of phone call use will provide the most relevant measure.

Example – phone calls are itemised on the bill

Julie has an $80 per month mobile phone plan, which includes $500 worth of calls and 1.5GB of data. She receives a bill that itemises all her

phone calls and provides her with her monthly data use.

Over a 4-week representative period, Julie identifies that 20% of her calls are work-related. She worked for the full income year and took 4

weeks of leave. Julie can claim a deduction of $177 in her tax return –

= monthly plan x 12 months / 52 weeks x number of weeks worked x work use %

= $80 x 12 months / 52 weeks x 48 weeks x 20%

= $177.23 rounded to $177

Example – non-itemised account

Ahmed has a prepaid mobile phone plan that costs him $50 per month. Ahmed does not receive a monthly bill so he keeps a record of his

calls for a 4-week representative period. During this 4-week period, Ahmed makes 25 work calls and 75 private calls. Ahmed worked for the

full income year, having had 3 weeks of leave.

Ahmed calculates his work use as 25% (25 work calls / 100 total calls x 100). He claims a deduction of $141 in his tax return –

= monthly plan x 12 months / 52 weeks x number of weeks worked x work use %

= $50 x 12 months / 52 weeks x 49 weeks x 25%

= $141.35 rounded to $141

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

45

Bundled phone and internet plans

Phone and internet services are often bundled. When claiming deductions for work-related use of one or more services, the costs must be

apportioned based on the work use for each service. The taxpayer will need to identify their work use for each service over a representative 4-week period. This will allow them to determine the pattern of use, which can then be applied to the full year. If other members in the

household also use the services, their use will need to be taken into account in the calculation.

For bundled plans, it is also necessary to identify the cost of each service covered by the plan. Bundled services can be apportioned:

• based on a supplier’s breakdown of relative costs of the bundled services,

• based on the relative costs of the bundled services as if they were purchased separately from the same supplier,

• based on information on a comparable supplier, or

• (if the above information is not available) by allocating the cost of the bundle equally across the number of services provided

Example – apportioning bundled services

Des has a $90 per month home phone and internet bundle, and unlimited internet use as part of his plan. There is no clear breakdown for

the cost of each service. By keeping a record of the calls Des makes over a 4-week representative period, he determines that 25% of his

calls are for work purposes. Des also keeps a record for 4 weeks of the data downloaded and determines that 30% of the total amount used

was for work. Des worked for the full income year and took 4 weeks of leave.

As there is no clear breakdown of the cost of each service, it is reasonable for Des to allocate 50% of the total cost to each service.

Step 1 – work out the value of each bundled component

Internet $45 per month ($90 / 2 services)

Home phone $45 per month ($90 / 2 services)

Step 2 – apportion the work-related use

Home phone

= $45 per month x 12 months / 52 weeks x 48 weeks x 25%

= $124.62 rounded to $125

Internet

= $45 per month x 12 months / 52 weeks x 48 weeks x 30%

= $149.54 rounded to $150

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

46

In his tax return, Des would claim a deduction of $275 ($125 + $150) for the year.

If, in the example above, the bill identified that the monthly cost of the phone service in his bundle is $30 and the internet service is $60 then

Des would use these amounts to calculate his deduction.

Where the telephone expenses claim is made as a consequence of working from home, a set rate may be able to be claimed, which will take

into consideration expenses incurred such as energy, mobile and home phone, internet, computer supplies and stationery (see Working from

Home), rather than calculating these items separately. The method used to claim should be the one that gives the highest claim, provided

the necessary records are available.

Tolls

A deduction is allowed for bridge and road tolls when incurred in the course of employment (not commuting). This is claimed at Item D2.

Tools Of Trade

Expenditure on repairing, sharpening and insuring tools of trade are deductible. The purchase cost of tools, where the amount does not

exceed $300, will be fully claimable in the year of purchase. This is subject to the Set and Multiples rule, which will be discussed in a later

module. Tools costing more than $300 each will have to be depreciated. Where a tool kit is purchased, even if individual tools in the kit cost

less than $300, the whole kit should be depreciated.

Vaccinations

A deduction is generally not allowed for vaccinations (even if required by an employer). There are some limited circumstances where

vaccinations may be tax deductible. This is where a taxpayer can prove the vaccination is to prevent a disease that is not one which affects

the general public.

Visa

The ATO take the view that Visa application fees are not generally deductible even if undertaking work related travel. As the employee

generally only commences work after entering the foreign country, these costs are incurred at a point too soon. However, pilots and other

airline employees, usually start flying from one country before possibly entering another country for which a visa is required. Thus, they have

commenced working as soon as they started flying from the first country, making the visa a requirement ‘in the course of their duties.’ For

these employees, visa costs will be deductible.

Watches

A deduction is not allowed for the cost of purchasing or repairing an ordinary wristwatch as the expense is generally considered private or

domestic. However, a deduction may be able to be claimed for the cost of purchasing or repairing a specialty watch that has the necessary

connection with the taxpayer’s income producing activity. Stop watches, fob watches and divers’ watches are allowed for relevant occupa-

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

47

tions; for example, a secretary cannot claim a stopwatch while an athletics coach can. A nurse may claim repairs and replacements on a

nurse’s fob watch.

A smart watch (that connects to a phone or other device to provide notifications, apps and GPS for example) is also a private expense, and

not deductible under ordinary circumstances. However, if some of the smart watch’s functions are required as an essential part of the taxpayer’s income-producing activity a deduction may be allowed. A diary will need to be kept to determine the taxable use percentage.

Wet Weather Gear

A deduction is allowed for wet weather gear when required to work out in the rain for extended periods or when handling hoses and/or

chemicals. These items will be deductible where they protect the wearer from the risk of serious illness or injury due to the work environment. These expenses are claimed at Item D3.

Working Dogs / Guard Dogs

The cost of maintenance of a working dog or a guard dog is a deductible expense. Amounts may be claimed for expenses incurred on food,

veterinary bills etc. The cost of acquiring and training a working dog is capital in nature and a deduction will be allowed for decline in value.

Working dogs are usually trained for their role from a young age and are not treated like pets. As with all other expenses, the dog must have

the necessary connection to earning income. Generally, it must be a requirement of your employment that you provide your own animal.

Examples where this deduction may be allowed:

• working dog of a truck driver transporting cattle

• working dog of agriculture workers herding livestock

• trained guard dog for guarding business premises

• certified therapy dogs used by qualified therapist

• police dog and security dog

• performing dogs

No deductions may be claimed for a pet dog.

Working With Children Check

The cost of a working with children check application is deductible in the following situations:

• the employee is an existing employee and is required to obtain a suitability notice in order to continue to earn assessable income in their

position

• a new employee has recently earned assessable income from being continuously employed within the field of child related employment.

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

48

Example

Freda received most of her income in the child-related employment field. For years, she has worked at a range of schools as a teacher,

employed under a series of temporary contracts. Her last contract ended in March 2023 and she accepted another contract at a different

school in May 2023. In order for Freda to start this new contract, the principal of the school is now required to apply for a suitability notice

for Freda. Freda pays the application fee for the suitability notice. Freda can claim the cost of the application as a deduction. Although she is

a new employee at this particular school, she has been continuously employed in a child-related employment field and the expense is

necessary to her employment.

The cost of getting the initial suitability notice for a new employee who has not recently been continuously employed in the field of childrelated employment is not deductible.

Working from home expenses

Where a taxpayer works from home they may be able to claim a deduction for the additional costs incurred in relation to this. These costs

may include:

• electricity or gas (energy expenses) for heating or cooling and lighting

• home and mobile phone expenses

• home and mobile internet or data expenses

• stationery and office supplies

• the decline in value of depreciating assets – for example

o office furniture such as chairs and desks

o equipment such as computers, laptops and software

• the repairs and maintenance of depreciating assets

• repairs to a dedicated office area

• cleaning of a dedicated office area

From the 2023 income year onwards there are two methods available to calculate the claim:

• Revised fixed rate method

The fixed rate method can be used to claim some of the expenses incurred when working from home.

• Actual cost method

The Actual Expenses method can be used to claim the work or business related portion of all of the above expenses, calculated

separately.

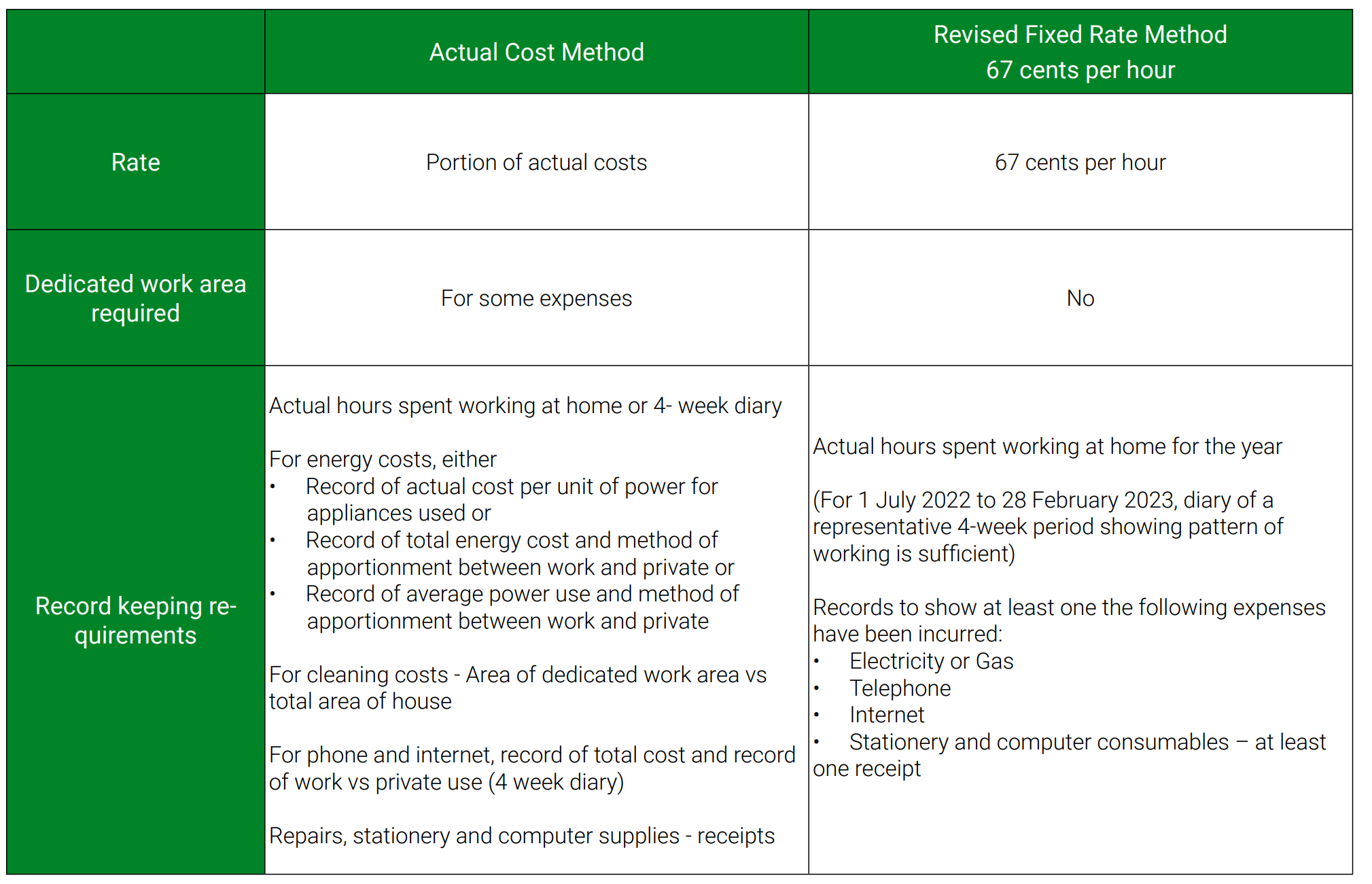

Revised Fixed Rate Method (PCG 2023/1)

The revised fixed rate method allows a taxpayer to claim 67 cents per hour they worked from home to cover the cost of the following

expenses:

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

49

• electricity or gas (energy expenses) for heating or cooling and lighting

• home and mobile phone expenses

• home and mobile internet or data expenses

• stationery and computer consumables (such as printer cartridges and paper)

The taxable use percentage of other expenses will be calculated and claimed separately. This includes:

• the decline in value of depreciating assets – for example

o office furniture such as chairs and desks

o equipment such as computers, laptops and software

• repairs and maintenance of depreciating assets

• cleaning of a dedicated office area

• repairs to a dedicated office area

It is not necessary to have a separate home office or dedicated work area to claim using the revised fixed rate method. If more than one

person in a household is working from home at the same time, each will be able to claim using this method.

In order to make this claim, the taxpayer must:

• Be working from home while carry out employment duties (or carrying on a business)

• Have incurred additional expenses as a result of working from home and

• Keep and retain relevant records in respect of the time spent working from home and for the additional running expenses.

The work from home must be substantive and directly related to the income producing activity. Minimal tasks, such as occasionally

checking emails or taking phone calls while at home, will not qualify as working from home for the purposes of claiming the fixed rate

method.

The taxpayer must also be able to demonstrate they have incurred additional running expenses such as energy, phone, internet, stationery

and computer consumables. To demonstrate these expenses have been incurred, one monthly or quarterly statement for the relevant

expense must be kept. If the bill is not in the taxpayer’s name, they will also have to keep additional evidence showing they incurred the

expense, such as a joint credit card statement showing payment or a lease agreement showing they share the property, and therefore the

expenses, with others. The ATO does not consider paying board as evidence that expenses have been incurred. To demonstrate that

expenses such as stationery and computer consumables have been incurred, one receipt for an item purchased must be kept.

It is not necessary to have incurred all of these expenses, but at least one of these types of expenses must have been incurred.

A record must be kept of the time spent working from home. For the 2023-24 and later income years, records must be kept for the entire

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

50

income year of the number of hours worked from home. An estimate for the entire income year or an estimate based on the number of

hours worked during a particular period and applied to the rest of the income year will not be acceptable.

The record of hours for the income year can be in any form, provided it is kept contemporaneously. That is, the records must be made as

close as practical to the time of the events. Acceptable records include:

• Timesheets

• Rosters

• Logs of time spent accessing employer systems or online business systems

• Time tracking apps

• A diary or similar document kept contemporaneously.

For the 2023 year, for the period 1 March 2023 to 30 June 2023, a record of the total number of actual hours worked from home must be

kept. However, for the period 1 July 2022 to 28 February 2023, it is only necessary to keep a diary record over a period of four weeks, which

is representative of the pattern worked during the whole period. This can be used to estimate the number of hours worked from home for

the whole of the 8 months (approximately 35 week) period.

The rate per hour calculates the total deductible expenses for energy, internet, mobile and home phone, and stationery and computer consumables for the income year.

This means no additional separate deduction can be claimed for any of these expenses. For example, if the taxpayer uses their mobile

phone when working from home and also when they are working from somewhere other than their home, the total deduction for mobile

phone expenses for the income year will be covered by the hourly rate of 67c per hour.

Claiming Expenses the Fixed Rate Method does not Include

In addition to the fixed rate method, a separate claim can be made for the taxable use percentage of expenses not included in this method,

such as the decline in value and repairs of depreciating assets (office furniture, computers, laptops, software etc).

Where there is a dedicated office area, the cost of cleaning and repairs to the office area may also be claimed. The amount that can be

claimed for these expenses is the amount that is reasonable in the circumstances. For example, the cost of repairing a broken window in a

doctor’s surgery is wholly deductible, while the cost of repairing a broken window in a home office which is used for both business and private purposes would have to be apportioned accordingly.

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

51

Actual Expenses Method

The Actual Expenses method can be used to claim the work (or business) related portion of all expenses incurred in running the home office, including:

• electricity or gas (energy expenses) for heating or cooling and lighting

• home and mobile phone expenses

• home and mobile internet or data expenses

• stationery and office supplies

• the decline in value of depreciating assets – for example

o office furniture such as chairs and desks

o equipment such as computers, laptops and software

• the repairs and] maintenance of depreciating assets

• repairs to a dedicated office area

• cleaning of a dedicated office area

In order to use this method for claiming energy costs, the additional expenditure must relate to facilities provided exclusively for the taxpayer’s benefit while they work. If a taxpayer merely sits in the lounge room with other members of the family (who are not working from home)

and at the same time does some work related activity, the expenditure for lighting and heating/cooling retains its private or domestic character. However, if the taxpayer uses a room at a time when others are not present (or the others present are also working from home) or

uses a separate room, they will be entitled to a deduction for the energy costs.

If another member of the household is also working from home in the same area of the house or using the same service as the taxpayer, the

expenses must be apportioned.

To calculate the taxable use percentage of energy costs, the taxpayer must keep a record of the number of hours worked from home during

the year or a diary record over a representative 4 week period to establish the usual pattern of working from home. In addition, they will need

to keep all receipts, bills and other documents which show the additional running expenses.

A record of the floor area of any dedicated home office compared with that of the whole house may be needed to apportion expenses such

as cleaning.

The record keeping for the actual cost method is much more stringent but will often result in a higher claim.

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

52

Heating, Cooling, Lighting and Running of Office Equipment

Method 1

Using the actual expenses method, the cost of power can be calculated using the following:

· cost per unit of power used (from utility bills)

· average units used per hour (which is the power consumption per kilowatt hour for each appliance, equipment or light used)

· total hours used for work-related purposes (from diary record)

Example

Jacinta works in her home office 15 hours per week. She ensures no one else is in the home office during this time. Jacinta has had 4

weeks holiday during the year, during which time she did not work.

While she is working in her home office, Jacinta operates the following equipment:

· desktop computer and two monitors (total power consumption is 200 Watts or 0.2 kW)

· lights (100 Watts or 0.1 kW)

· air conditioner (300 Watts or 0.3 kW)

Her power bill shows that Jacinta pays 26 cents per kWh for her power.

Jacinta has worked for 720 hours from home during the year (15 hrs per week x 48 weeks). The actual cost of running her office equipment

while she is working is:

= 720 hours x 0.6 kW x 26 cents per kWh

= $112.32

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

53

Method 2

Alternatively, the ATO will accept a bona fide estimate based on a reasonable percentage of the household annual fuel bill. As such, a more

practical method of calculating power usage is to use the average daily cost of the household fuel bill (available from utility accounts) or the

total cost of the household fuel bill for the year and claim the percentage of this that relates to the running expenses of the home office.

Example

In the above example, Jacinta estimates that, of the electricity being used in the house while she is working in the home office, 60% would

be a reasonable estimate of personal usage for items such as refrigerator, TV on standby etc.

Jacinta’s electricity bill shows that her average daily cost is $9.20 per day.

Average cost of power per hour = $9.20 / 24 hours = 38.33 cents per hour.

Jacinta works from home for 720 hours during the year. The estimated cost of this is:

= 720 hours x 38.33 cents per hour x 40%

= $110.39

Jacinta’s total fuel bill for the year is $3,358

= $3,358 x 720 hours / 8,760 hours x 40%

= $110.40

Claiming Expenses other than Heating, Cooling and Lighting (Actual Costs Method)

When using the actual expenses method, in addition to heating, cooling and lighting expenses, a separate claim can be made for the taxable

use percentage of phone, internet, stationery, computer consumables, decline in value and repairs of depreciating assets (office furniture,

computers, laptops, software etc).

Where there is a dedicated office area, the cost of cleaning and repairs to the office area may also be claimed. The amount that can be

claimed for these expenses is the amount that is reasonable in the circumstances.

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

54

Example: Cleaning of Office Area

Jacinta paid a cleaner $6,240 during the year to clean her house (including her dedicated office area).

Jacinta has supplied the following information:

Floor area of the home office 12m2

Floor area of the whole house 60m2

Number of hours per week the home office is used by Jacinta for work purposes 15 hrs

Number of hours per week the home office is used by Jacinta for private purposes or by other members of the household 50 hrs

Jacinta can claim a deduction for the cleaning of her office:

=total cost x floor area of home office / total floor area x hours used for work / total hours used

= $6,240 x 12m2 / 60 m2 x 15 hours / 65 hours

= $288.00

Expenses that cannot be claimed when working from home

Irrespective of which method is used for calculating a deduction for working from home expenses, the following expenses cannot be

claimed:

• the cost of coffee, tea, milk and other general household items the employer may have otherwise provided at work

• costs related to children and their education, including setting them up for online learning, teaching them at home or buying equipment

for them such as iPads and desks

• expenses that have been reimbursed or paid for directly by the employer

• decline in value of items provided by the employer

• time spent not working, such as time spent home schooling children or lunch breaks.

Choosing the method to use

Taxpayers can choose the method that provides the greatest deduction, provided they have the necessary records.

Taxpayers working in the same household at the same time do not have to choose the same method – they can each choose the method

that will benefit them the most. If a taxpayer chooses to use the actual expenses method, they will need to ensure they have applied an

appropriate apportionment methodology which isolates their individual component of expenses.

If using the set rate method, the full 67 cents per hour will apply to all taxpayers in the household, providing they have contributed to at least

one of the expenses covered by this method and the have the necessary documentation.

Summary of working from home claim methods

PRIOR YEAR HOME OFFICE CLAIMS

If preparing prior year tax returns, home office expenses can be claimed using one of the following methods:

• Fixed Rate Method: a deduction can be calculated at a rate of 52 cents for each hour worked from home. This rate applied from 1 July

2018 to 30 June 2022 and covers the costs of:

o electricity and gas for cooling, heating and lighting

o the decline in value and repair of home office furniture and furnishings, and

o the cost of cleaning the home office.

In order to use this method, it is necessary to have a dedicated work area. A diary record over a representative 4-week period is required to

establish the number of hours worked from home during the year.

Other expenses, such as telephone, internet and decline in value of computer and other office equipment, stationery and computer supplies

can be claimed separately.

• Shortcut Method: for the period 1 March 2020 to 30 June 2022, a deduction can be calculated at the rate 80 cents for each hour worked

from home. This method includes an allowance for the cost of all expenses incurred when working from home (energy, telephone,

internet, depreciation and repairs of office furniture and equipment, stationery and computer consumables and cleaning of the home

office). It is not necessary to have a dedicated work area in order to use this method. If claiming using this method, no additional

expenses can be claimed.

• Actual Cost Method: a deduction for a proportion of actual expenses incurred (as above).

Where the home is a place of business (NOT for personal services income – covered in a later module)

Where a taxpayer has an area of their home set aside as a ‘place of business’, they may be able to claim a deduction for occupancy

expenses, as well as the running expenses, to the extent they relate to their income producing activity. Occupancy expenses include:

• mortgage interest or rent

• council and water rates

• land taxes

• house insurance premiums

The following factors may indicate that an area in the home has the character of a place of business:

• the area is clearly identifiable as a place of business

• the area is not readily adaptable for use for private or domestic purposes in association with the home generally

• the area is used exclusively or almost exclusively for business purposes

• the area is used regularly for visits by clients or customers

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

58

An area in the home may also have the character of a place of business if it can be shown that an area is used as the sole base of operations for an income producing activity. In order to satisfy this criterion, the taxpayer must show that:

• it is a requirement inherent in the nature of the taxpayer’s activities that they have a place to work

• the taxpayer has no alternative place of work (or business)

• an area of the home is used exclusively or almost exclusively for income producing purposes.

Where an employer provides an office for the employee to work from, their home will not generally be considered a place of business, even if

they are required to work outside normal business hours or choose to work from home.

Where an individual is working from home temporarily only due to the coronavirus, the ATO has advised they will not be eligible to claim occupancy expenses.

Examples of taxpayers that may be able to claim occupancy expenses

• an architect who has a private practice at their home

• a music teacher who conducts lessons from home

• a full-time scriptwriter who conducts writing activities from home

• a clergyman who has set aside a room in the home as an administration centre and used for discussing problems with parishioners

• a sales representative who is required to maintain an office in their own home to carry out their work duties

• a computer consultant who works from home

• a tradesman with a workshop at their home

Occupancy expenses are apportioned on a floor area basis as follows:

=floor area related to income earning activity/total floor areax100

Where a taxpayer has an area of their home set aside as a ‘place of business’, their running expenses can be calculated using either the

fixed rate method or the actual expenses method. If using the actual expenses method, floor area can be used to as a basis of apportionment.

Example

Sara is a sole trader and operates her small business from her spare room. This room is used exclusively for her business. The floor area of

this room is 10m2 and the floor area of the house is 250m2.

Sara’s electricity and gas bills for the year totalled $3,175. Sara can calculate her deduction for these costs as follows:

Section 01

Section 02

Section 03

Section 04

Section 05

Section 06

59

= total cost x floor area %

=$3,175 x 4%

= $127

This type of claim is generally not available for employees.